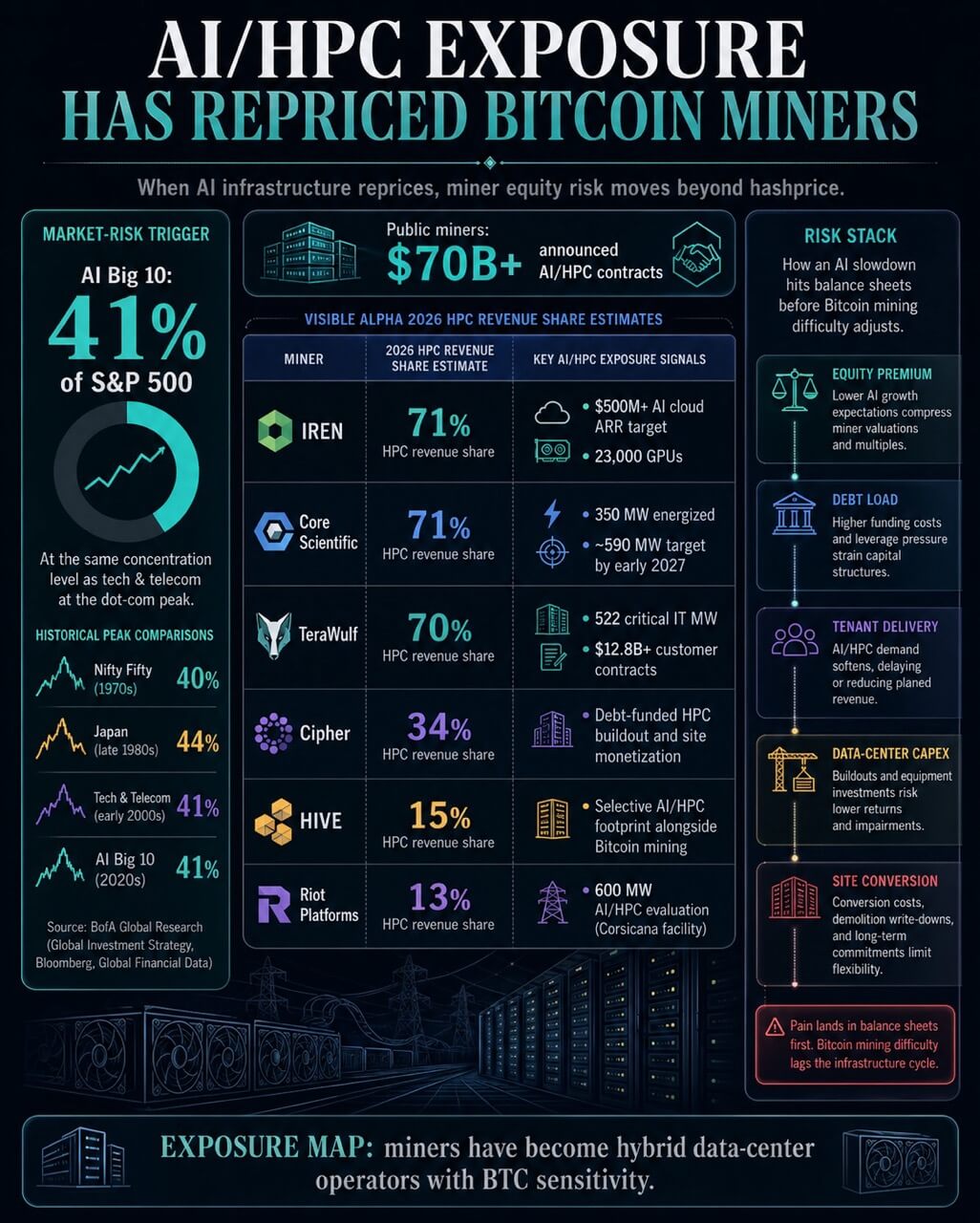

The ten largest AI shares now make up about 41% of the S&P 500, in keeping with a BofA World Analysis chart circulated on-line.

That places the AI basket on the identical focus degree that tech and telecom reached across the dot-com peak. The BofA chart put the Nifty Fifty at 40% within the Nineteen Seventies and Japan at 44% within the late Eighties.

The comparability turns a stock-market focus warning right into a stress take a look at for a nook of crypto that has spent the previous yr promoting traders a brand new identification.

The market focus is the stress set off. Miner disclosures and mining reviews provide the publicity map.

Public Bitcoin miners more and more commerce as hybrid infrastructure corporations with BTC publicity. Many have signed AI or high-performance computing contracts, raised capital for denser knowledge facilities, transformed premium energy websites, or shifted investor consideration towards long-term lease economics.

If the AI infrastructure premium fades, these corporations face a unique sort of strain. The chance strikes from hashprice alone into debt, contract sturdiness, building execution, and fairness multiples.

On the identical time, Bitcoin will get a second-order take a look at. A weaker AI buildout may ease the scramble for energy, rack house, interconnections, cooling tools, and GPUs.

That will harm miners whose new valuations depend upon AI progress, whereas presumably serving to remaining miners if scarce infrastructure turns into simpler to safe.

Miners Have Repriced Themselves Round AI

The miner pivot is now measurable in income forecasts. A projected income combine cited by S&P World Market Intelligence confirmed listed miners, together with IREN, Riot Platforms, Core Scientific, HIVE, Cipher, and TeraWulf, shifting into AI and HPC workloads.

The projected income combine is already massive sufficient to alter how these corporations are assessed.

Seen Alpha anticipated HPC to account for 71% of 2026 income at IREN and Core Scientific, 70% at TeraWulf, 34% at Cipher, 15% at HIVE, and 13% at Riot.

That unfold exhibits the sector has break up into cohorts. Some miners have gotten data-center operators with Bitcoin publicity.

Others are preserving mining because the core enterprise whereas preserving AI optionality at websites which have energy and grid entry.

The dimensions exhibits up in miner economics. Public miners have introduced greater than $70 billion in mixture AI/HPC contracts, in keeping with CoinShares.

The agency additionally stated WULF, Core Scientific, Cipher, and Hut 8 are successfully turning into data-center operators that also mine Bitcoin.

That adjustments the market hyperlink from an AI inventory selloff. A falling AI a number of would circulation by means of miner equities as a result of traders have assigned worth to the HPC pipeline.

Decrease AI demand would additionally strain the financing case for tasks constructed round long-duration tenants, higher-density cooling, and premium grid positions.

Mining margins would nonetheless depend upon BTC value and issue, however the fairness case would have one other variable.

The leverage knowledge factors in the identical path. CoinShares stated a number of miners had taken on massive debt hundreds for AI buildouts, together with $3.7 billion in convertible notes at IREN, $5.7 billion in complete debt at WULF, and $1.7 billion in senior secured notes issued by Cipher.

mycryptopot has individually tracked how miners have been funding the AI pivot with debt whereas promoting BTC. Put merely, the AI pivot has added a credit score cycle to a enterprise that already lived with a Bitcoin cycle.

The desk under mixes 2026 income estimates, 2025 firm disclosures, and contract updates, so every row alerts publicity throughout totally different time horizons.

| Miner | AI/HPC publicity sign | Repricing strain level |

|---|---|---|

| Core Scientific | Seen Alpha projected 71% HPC income share in 2026 | CoreWeave supply, customer-funded capex, conversion execution |

| TeraWulf | 522 crucial IT MW underneath long-term leases | Financing, tenant timelines, and credit-enhanced contract supply |

| IREN | AI cloud ARR goal above $500 million from 23,000 GPUs | GPU contract length, utilization, tools economics |

| Riot | 600 MW Corsicana AI/HPC analysis | Worth of utilizing premium energy for AI versus mining |

| Cipher | Seen Alpha projected 34% HPC income share in 2026 | Debt-funded HPC buildout and web site monetization |

Cipher’s rebrand towards HPC provides one other instance of the shift. TeraWulf’s Fluidstack growth exhibits how miners have paired massive energy portfolios with AI tenants and credit score help.

The Danger Is In The Websites, Contracts, And Capital Stack

Core Scientific is the clearest instance of the shift from mining sensitivity to infrastructure execution. In its fourth-quarter 2025 outcomes, the corporate stated it had energized about 350 MW underneath its CoreWeave contract and remained on monitor to ship about 590 MW by early 2027.

It additionally reported that This fall colocation income rose to $31.3 million from $8.5 million a yr earlier, whereas digital asset self-mining income fell to $42.2 million from $79.9 million.

That’s the pivot in working kind. Energy and buildings as soon as tied primarily to Bitcoin manufacturing are being monetized by means of colocation.

Core Scientific additionally stated $226.2 million of its $279.2 million in fourth-quarter capital expenditures was funded by CoreWeave underneath current agreements. That buyer funding reduces some capital pressure, however it additionally exhibits how deeply the buildout depends upon an AI tenant’s progress path.

The conversion additionally introduces accounting complexity. Core Scientific stated it was restating prior monetary statements after figuring out improper capitalization of property dedicated to demolition throughout facility conversion from mining to HPC colocation infrastructure.

The difficulty was company-specific, however it illustrates a broader level. Shifting from mining halls to high-density AI infrastructure goes past advertising and marketing language.

Core Scientific’s canceled CoreWeave merger settlement exhibits that AI-linked worth already sits inside shareholder choices.

CoreWeave’s 2025 Kind 10-Okay provides counterparty context, together with massive contracted energy commitments and disclosed dangers tied to AI demand.

The miner publicity is, due to this fact, linked to each web site supply and the monetary well being of the AI cloud ecosystem.

TeraWulf exhibits the identical shift at a bigger contracted scale. In its full-year 2025 outcomes, the corporate reported long-term knowledge heart lease agreements totaling 522 crucial IT MW, greater than $12.8 billion in long-term credit-enhanced buyer contracts, and $6.5 billion in long-term financings.

It stated HPC internet hosting had turn into its major progress engine whereas it continued to function legacy mining infrastructure opportunistically.

CoinShares reported that WULF mined 262 BTC in This fall alongside $9.7 million in HPC lease income. The identical report stated WULF’s cost-per-BTC figures had been distorted by the corporate’s transition, together with curiosity, SG&A, and depreciation linked to the brand new infrastructure base.

That distinction is essential. As soon as a miner turns into an AI infrastructure firm, per-BTC value metrics can distort the enterprise until the steadiness sheet is separated from the remainder of the mining fleet.

Riot’s Corsicana choice exhibits how AI optionality can alter Bitcoin’s capability path earlier than a last AI contract even exists. The corporate’s Corsicana replace stated it was evaluating AI/HPC makes use of for about 600 MW of remaining energy capability, halting a beforehand introduced 600 MW Part II Bitcoin mining growth, and slicing anticipated year-end 2025 self-mining capability from 46.7 EH/s to 38.4 EH/s.

IREN provides a unique publicity sort. Its October 2025 AI cloud replace focused greater than $500 million in annualized AI cloud income from 23,000 GPUs by the tip of Q1 2026, with 11,000 GPUs contracted for about $225 million of ARR on common two-year phrases.

That creates a quicker repricing channel than long-term colocation. GPU cloud economics can shift as {hardware} provide, utilization, and buyer budgets change.

Energy Shortage Units Bitcoin’s Facet Of The Commerce

The Bitcoin aspect of the commerce is much less direct. A weaker AI infrastructure cycle would first strain AI-exposed miners by means of fairness valuation, funding prices, and contract expectations.

Bitcoin’s community would really feel the change by means of the economic base that competes for a similar energy and websites.

The AI-mining hyperlink is bodily. Bitcoin mining stays the bigger mixture income pool in key BTC value situations, whereas AI has turn into a direct financial threat to the community’s industrial safety base.

AI and mining compete for land, grid interconnections, substations, cooling design, financing, and administration consideration.

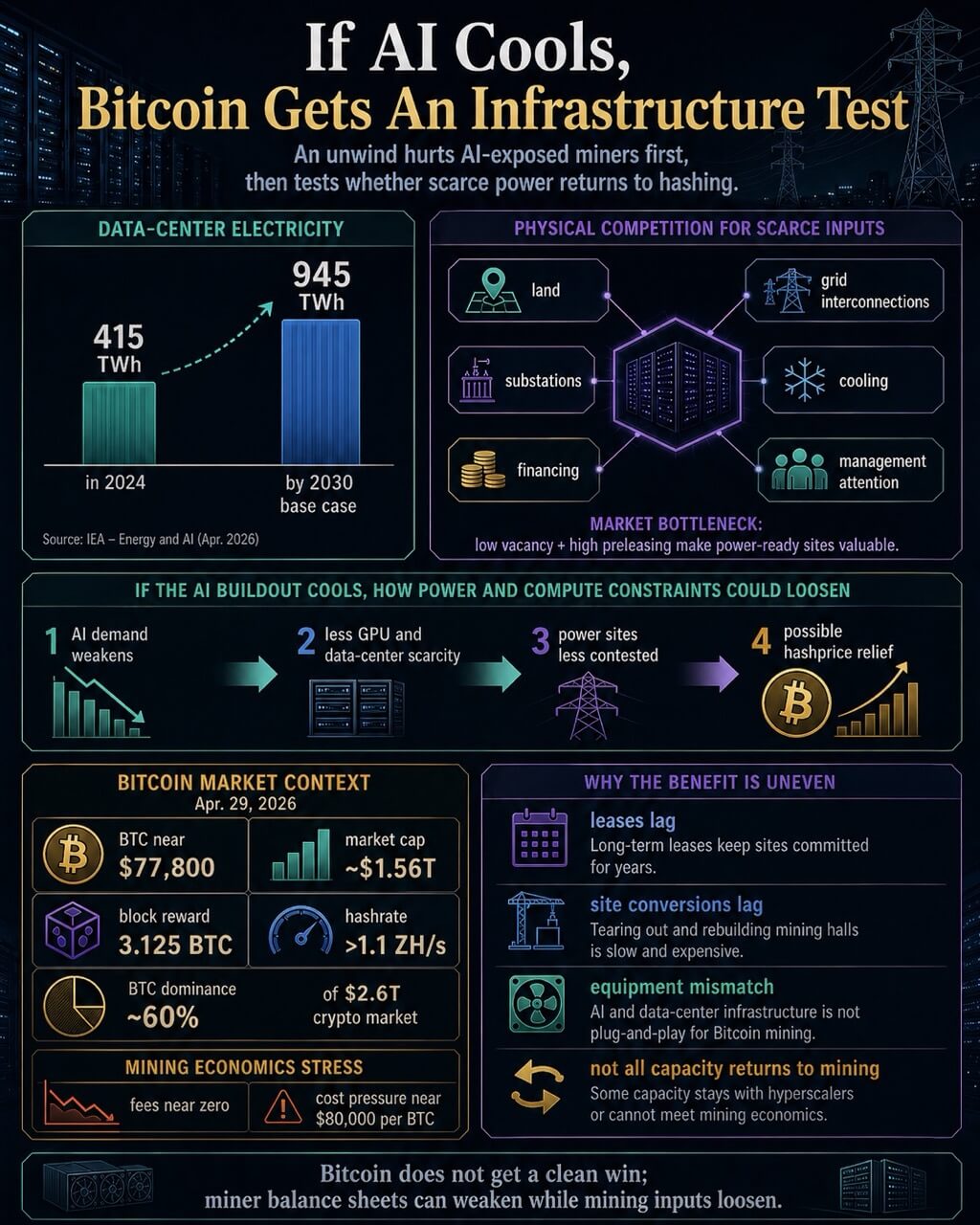

Vitality demand from AI explains why the competitors is sturdy. The IEA estimated that knowledge facilities consumed about 415 TWh of electrical energy in 2024 and projected that world data-center consumption would roughly double to 945 TWh by 2030 in its base case.

AI-driven accelerated servers account for a serious share of the rise. Knowledge facilities might be constructed quicker than energy techniques can add transmission, substations, and era, which makes location and grid entry precious.

A North America data-center developments report provides the market bottleneck behind that argument. Low emptiness and excessive preleasing make power-ready capability extra precious.

For miners, the scarce asset is usually the energized web site, with the ASIC fleet just one a part of the stack.

As of press time, Bitcoin market knowledge present BTC buying and selling close to $76,800, with a market cap of round $1.5 trillion, a present block reward of three.125 BTC, and a community hashrate above 1.1 ZH/s.

mycryptopot’s mixture market web page exhibits Bitcoin’s dominance at round 60% of the $2.6 trillion crypto market. These figures put miner economics underneath strain even earlier than AI competitors is taken into account.

BTC value, charges, issue, and power prices nonetheless decide how a lot safety Bitcoin can help.

A cooling AI cycle may ease one a part of that strain. If hyperscaler demand, GPU shortage, or data-center preleasing weaken, miners that stayed nearer to Bitcoin may discover energy websites and infrastructure much less contested.

Issue may alter if capability exits mining, elevating hashprice for remaining operators. That mechanism seems in mycryptopot’s evaluation of miners as AI utilities.

That reduction has limits. The charge and value image retains the upside certified, with charges close to zero and value strain close to $80,000 per BTC.

Issue reduction alone leaves weak miner economics unresolved. Lengthy-term AI leases, customer-funded buildouts, interconnection agreements, tools specialization, and web site conversion prices additionally create lag.

An AI unwind would launch capability inconsistently, and a few of it might stay unusable for mining at engaging returns.

Two Outcomes Rely On AI Demand

The market threat signaled by the AI focus chart results in two totally different outcomes for miners.

Within the first, AI demand holds. Public miners with high-quality energy campuses hold signing HPC contracts as a result of AI tenants can provide longer income visibility than Bitcoin mining.

Premium websites hold drifting towards AI, whereas mining concentrates round versatile energy, demand response, stranded power, and geographies the place interruption is appropriate.

In that state of affairs, public miner equities turn into much less dependable proxies for BTC as a result of enterprise worth comes from leases and data-center execution as a lot as mined Bitcoin.

Within the second, AI infrastructure costs. The miners most uncovered to AI progress face strain by means of leverage, fairness multiples, contract assumptions, and building pipelines.

Debt raised for data-center buildouts turns into tougher to hold if anticipated AI returns fall. GPU cloud contracts with shorter phrases can reset quicker.

Lengthy-term colocation leases might provide extra safety, though additionally they lock websites right into a path that will take years to reverse.

Bitcoin’s doable profit sits downstream from that harm. The upside is a loosening of scarce inputs, decrease competitors for energy, and a greater hashprice setting for operators nonetheless targeted on mining.

It’s an industrial-security argument, with BTC value sitting exterior the direct declare.

That’s the reason the AI focus chart belongs in a dialogue of Bitcoin-miner steadiness sheets. The chart raises the likelihood that the AI commerce has turn into crowded.

The miner knowledge exhibits which crypto corporations have constructed round that commerce. The unresolved take a look at is whether or not these AI/HPC contracts stay sturdy sufficient to justify the shift, or whether or not the identical infrastructure that pulled public miners away from Bitcoin turns into a supply of stress.

For Bitcoin, the outcome can be combined as an alternative of fresh. A repricing may weaken a number of the best-capitalized public miners whereas making power and data-center inputs much less scarce for the miners that stay.

The subsequent sign will come much less from AI rhetoric than from financing phrases, tenant supply schedules, new energy contracts, and hashprice. These are the variables that can present whether or not miners purchased a stronger enterprise mannequin or imported a second cycle into Bitcoin’s safety base.