On Technique’s Could 5 earnings name, Technique CEO Phong Le stated plainly that “we’ll promote Bitcoin when it’s advantageous to the corporate,” with Saylor including that Technique would “most likely promote some Bitcoin to fund a dividend simply to inoculate the market.”

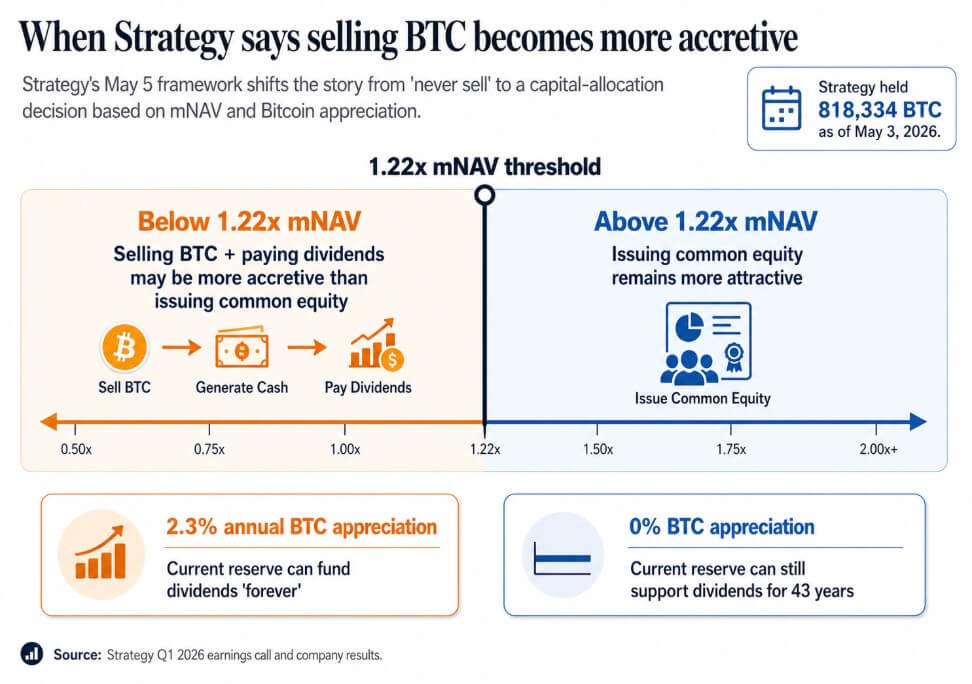

Technique held 818,334 BTC as of Could 3, up 22% year-to-date, with a market worth of $64.14 billion.

What the Could 5 name established was the general public normalization of BTC gross sales as a company finance lever and the quantitative framework now sitting behind it

Beneath roughly 1.22x mNAV, administration stated promoting BTC and paying dividends may be extra accretive than issuing frequent fairness. Saylor argued that if Bitcoin appreciates by simply 2.3% yearly, Technique’s present reserve can fund dividends “eternally,” and if Bitcoin appreciates at zero, the reserve can nonetheless assist dividends for 43 years.

The absolutist slogan gave solution to a mannequin through which firms that purchase when accretive, difficulty fairness when accretive, difficulty preferreds when accretive, and promote BTC when accretive are leveraged treasury-and-credit automobiles.

Traders initially purchased these firms as Bitcoin proxies constructed on shortage and permanence. The 1.22x mNAV threshold and the two.3% breakeven fee are a extra sincere model of that pitch, and a extra sophisticated one.

Technique to “promote some Bitcoin” after posting $12.7 billion Q1 loss as Saylor factors to $5 billion Bitcoin achieve

The corporate’s BTC Acquire metric is colliding with Wall Avenue forecasts for a first-quarter loss tied to Bitcoin’s drawdown.

When Bitcoin turns into liquidity

Sequans reported first-quarter income down 24.8% yr over yr to $6.1 million, alongside a $50.5 million working loss. The primary quarter included $11.7 million in realized web losses from Bitcoin gross sales, with proceeds primarily allotted to convertible debt redemption and an ADS buyback program.

As of Mar. 31, it held 1,514 BTC, with 1,217 BTC serving as collateral in opposition to $66.2 million of convertible debt. By Apr. 30, it held 1,114 BTC, with 817 BTC serving as collateral in opposition to $35.9 million of debt due by June 1.

This follows the identical sample as in November 2025, when Sequans offered 970 BTC to redeem 50% of its convertible debt, decreasing that obligation from $189 million to $94.5 million.

Over two quarters, when income falls and debt comes due, Bitcoin turns into operational liquidity. The pledged collateral construction commits BTC that the corporate nominally holds as collateral in opposition to obligations earlier than any sale resolution.

Sequans operates at a distinct scale from Technique, with a weaker working enterprise behind its treasury place. When BTC has to fund speedy debt service, stock logic takes over.

MARA utilized the identical logic in March on a bigger scale, promoting 15,133 BTC for roughly $1.1 billion and utilizing the proceeds to repurchase convertible notes, thereby reducing excellent convertible indebtedness by about 30% and capturing roughly $88.1 million in worth.

MARA packaged the transfer as stability sheet optimization pushed by debt construction and financing situations, establishing that BTC gross sales can arrive as capital allocation selections impartial of Bitcoin conviction, and that the related query for treasury firms is below what situations promoting turns into the highest-return transfer.

| Firm | BTC motion | Dimension of sale / holdings impression | Why BTC was used | What it alerts |

|---|---|---|---|---|

| Technique | Publicly normalized potential BTC gross sales | Held 818,334 BTC as of Could 3 | May promote BTC to fund dividends if extra accretive than issuing fairness | BTC is now a part of the corporate-finance toolkit, not only a reserve asset |

| Sequans | Offered BTC whereas below working and debt strain | BTC holdings fell from 1,514 on Mar. 31 to 1,114 on Apr. 30 | Debt redemption and ADS buyback | BTC turns into liquidity when income weakens and debt matures |

| MARA | Offered BTC for legal responsibility administration | Offered 15,133 BTC for about $1.1B | Repurchase convertible notes, reduce debt by about 30% | BTC gross sales may be framed as balance-sheet optimization, not simply misery |

What the shift decides

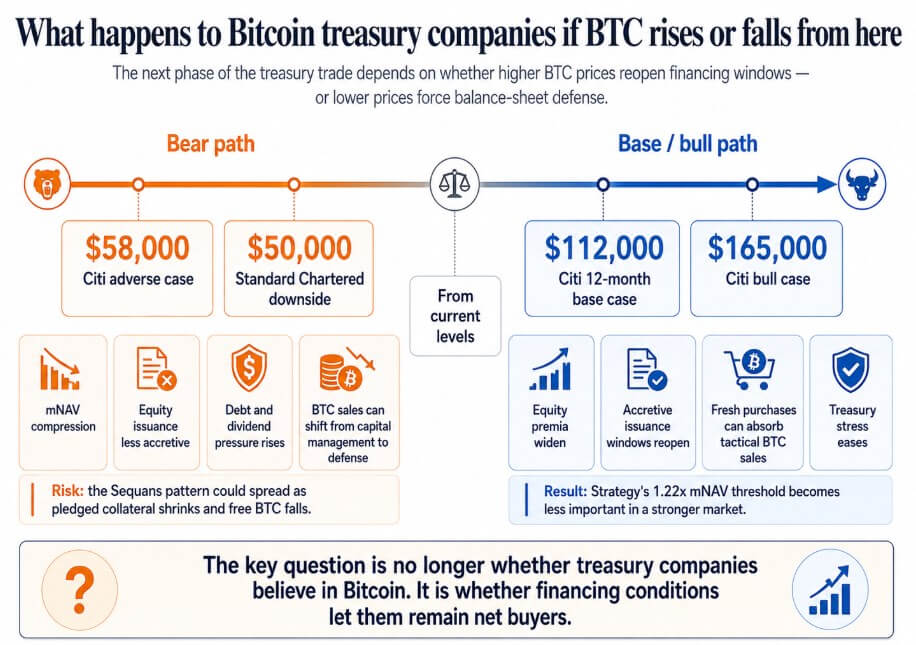

If Bitcoin recovers towards Citi’s 12-month base-case goal of $112,000 or its bull case of $165,000, fairness premia throughout treasury firms widen, accretive issuance home windows reopen, and bigger contemporary purchases take up tactical BTC gross sales.

Technique’s 1.22x mNAV threshold fades right into a technical element, and Sequans-type corporations that confronted debt stress by way of a weak Bitcoin market resolve their obligations and maintain unrestricted BTC heading into the subsequent cycle.

If Bitcoin strikes towards Citi’s $58,000 antagonistic case, which Customary Chartered has flagged as a possible path to $50,000, firms buying and selling close to or beneath NAV lose accretive entry to fairness markets.

On this state of affairs, most popular dividend obligations compound, and BTC gross sales transfer from capital administration to stability sheet protection.

The Sequans sample might unfold to any treasury firm that mixed skinny working income with BTC-backed borrowing, the place promoting Bitcoin to service debt whereas pledged collateral shrinks the free float turns into the one obtainable response.

At that time, the company Bitcoin bid turns right into a cycle through which falling costs set off extra promoting, pushing costs decrease.

The company Bitcoin treasury commerce rested on the promise of everlasting accumulation, which made these firms legible to traders as proxies for Bitcoin.

As soon as promoting turns into an acknowledged instrument contained in the mannequin, traders have to cost in debt maturities, collateral necessities, dividend obligations, and the mNAV thresholds at which administration might determine promoting outperforms issuing fairness.

Saylor’s 2.3% appreciation breakeven and 1.22x mNAV threshold are extra sincere. The following part of the Bitcoin treasury commerce shall be determined as a lot by financing situations as by Bitcoin conviction.