Welcome to our institutional e-newsletter, Crypto Lengthy & Brief. This week:

- Alec Beckman on why $BTC-backed lending just isn’t a crypto story, however a capital effectivity story.

- Serena Sebastiani on how stablecoins aren’t a crypto product; they’re changing into the settlement infrastructure world finance forgot.

- High headlines establishments ought to take note of by Francisco Rodrigues.

- “Ethena’s Solana lending markets cross $1B in 4 days” in Chart of the Week.

Thanks for becoming a member of us!

-Alexandra Levis

Skilled Insights

Bitcoin-backed loans belong within the cost-of-capital dialog

By Alec Beckman, VP of the Americas, Psalion

The argument just isn’t about whether or not to purchase bitcoin or not. It’s for advisors, actual property traders, small enterprise house owners and founders who already personal it, or work with purchasers who do. The sensible query is straightforward: if a shopper carries significant debt, why is $BTC-backed lending not within the capital stack dialogue? Debt-heavy professionals already evaluate collateral, price, charges, pace and covenants. Bitcoin-backed loans must be evaluated the identical approach.

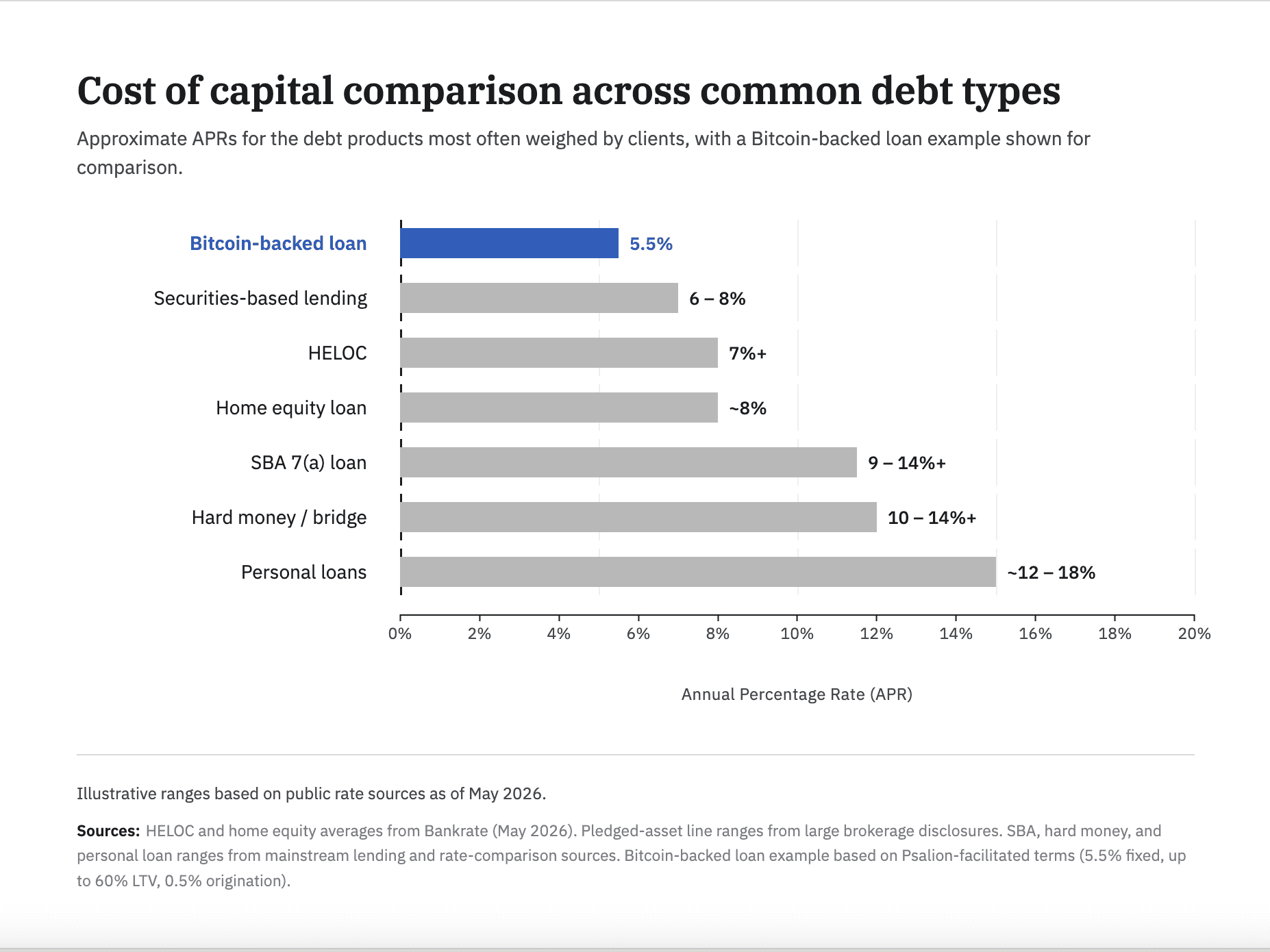

The debt menu is acquainted. HELOCs are tied to house fairness, usually variable, and at present sit above 7% for a lot of debtors. Arduous cash and bridge loans can transfer rapidly, however usually worth round 10% to 14% plus factors. Securities-based lending might be environment friendly, however charges usually start round 6% to eight% and require sizable brokerage property in a single place. Private loans steadily land within the low-to-mid teenagers. SBA loans might be helpful, however the all-in value, documentation and time to fund should not trivial.

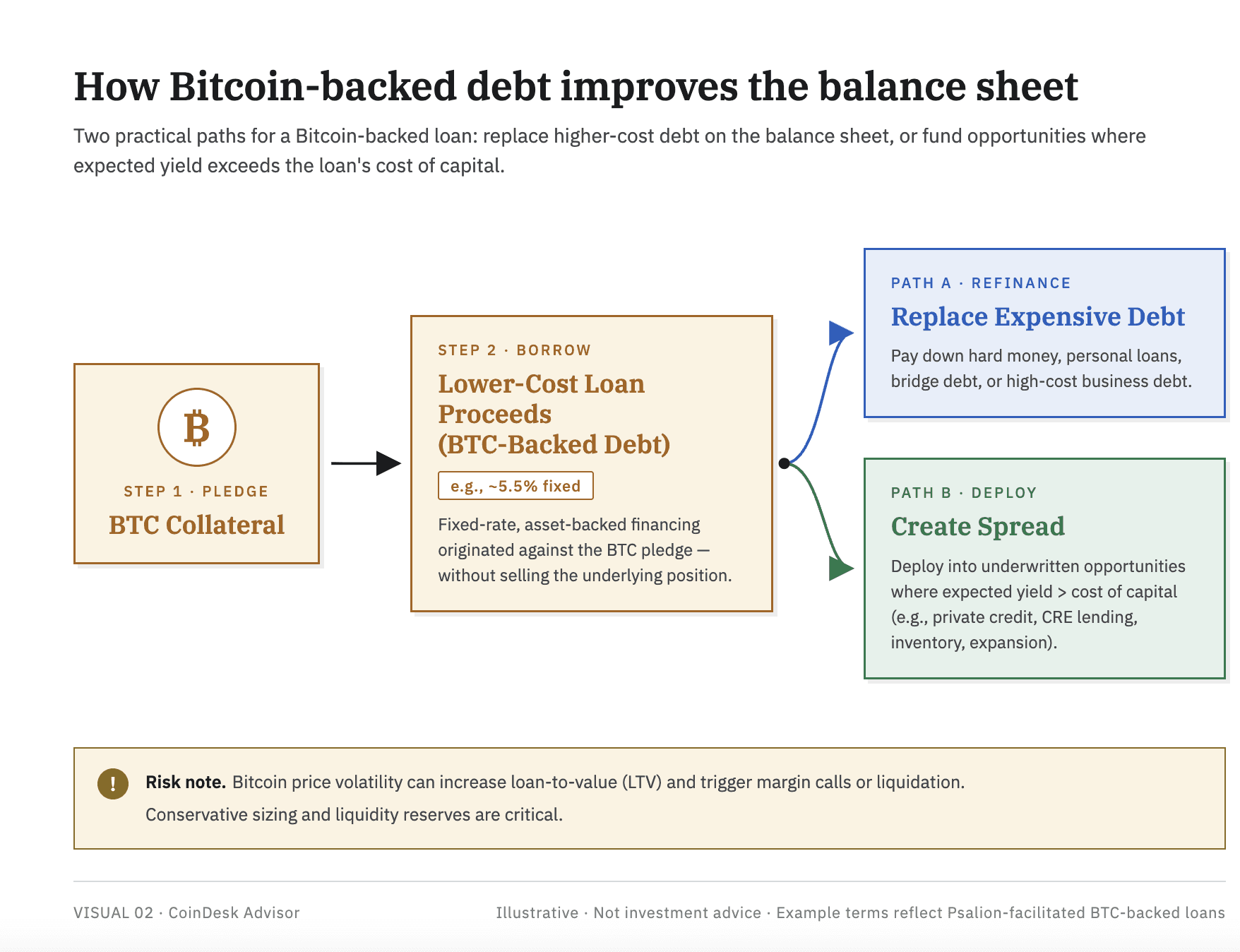

Bitcoin-backed lending modifications the collateral, not the mathematics. The borrower pledges $BTC, receives {dollars} or stablecoins and repays underneath agreed phrases. The asset is liquid, verifiable and straightforward to observe. Market charges nonetheless differ extensively, however extra aggressive constructions are rising. At Psalion, for instance, we facilitate entry to Bitcoin-backed loans at a 5.5% mounted price, as much as 60% LTV, with a 0.5% origination price. That’s one information level, however it exhibits why the class belongs in a severe debt comparability.

Price issues first. For somebody already holding $BTC, the related query just isn’t “Ought to I borrow?” It’s “The place ought to I borrow?” In opposition to a home? A enterprise? A securities portfolio? Or $BTC? If $BTC collateral produces cheaper capital than the borrower’s current debt, it may scale back the blended value of capital.

Charges matter subsequent. Arduous cash can carry factors on origination. SBA constructions can embody assure charges, closing prices and advisory prices. Private loans might embed greater APR by origination. Decrease price bitcoin-backed lending could make the all-in economics materially cleaner.

Friction issues too. Conventional credit score usually requires revenue verification, tax returns, value determinations, working statements, private ensures, covenants and time. $BTC-backed lending is collateral-first. The collateral might be verified rapidly and monitored repeatedly. Quicker entry to liquidity is not only comfort. It might probably change the economics of a refinance, acquisition, tax cost or bridge want.

Advisors ought to care as a result of $BTC is now a part of extra shopper steadiness sheets. Too usually, $BTC sits idle whereas the identical shopper pays greater charges elsewhere. If the shopper can borrow in opposition to $BTC and substitute dearer debt, the advisor has improved the steadiness sheet with out forcing a sale and probably making a taxable acquire.

There’s a second use case: yield on unfold. Some actual property traders, founders and enterprise house owners see alternatives the place anticipated returns exceed their value of capital, reminiscent of personal credit score, industrial actual property lending, stock or working growth.

Borrowing in opposition to $BTC to pursue these alternatives could make sense when the borrower understands each side of the commerce: the yield alternative and the collateral threat.

That threat is actual. Bitcoin is unstable. If the worth falls sufficient, LTV can breach agreed thresholds and set off margin calls or liquidation. Liquidation can create a taxable occasion. This isn’t for each shopper. It’s for debtors who perceive $BTC volatility, keep liquidity and dimension loans conservatively beneath most LTV.

For purchasers who already personal bitcoin and already carry debt, $BTC-backed lending just isn’t a crypto story. It’s a capital effectivity story. Ignoring it might imply leaving cheaper capital, or a priceless unfold alternative, on the desk.

Principled Views

Stablecoins are actually infrastructures

By Serena Sebastiani, chief technique officer and head of presidency and regulatory affairs, Fuze

There is a form of monetary friction that turns into invisible whenever you stay inside it lengthy sufficient.

From New York or London, cross-border funds work. From Nairobi, Jakarta or Almaty, they don’t.

An SME in Nairobi pays a provider in Karachi. The cash leaves Monday. It arrives Thursday. Alongside the best way it passes by two correspondent banks, absorbs charges on each ends, will get hit with an FX unfold on the USD conversion and triggers a number of compliance checks. Each the client and the provider soak up the friction by pricing it into the deal and lengthening the credit score word.

That is the way it truly works to function throughout the fastest-growing commerce corridors globally: Gulf to South Asia, intra-African commerce, CIS to MENA, and Southeast Asia remittances.

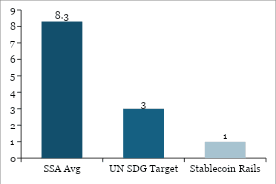

Multiply that by the $136 billion SME commerce finance hole in Africa alone. Multiply it by the $100 billion in annual remittances flowing into the continent. Multiply it throughout the Gulf-to-South-Asia hall, CIS-to-MENA and intra-ASEAN. And likewise account for the price of sending cash into Sub-Saharan Africa, which stays the costliest area on this planet, at 8.3% on common (nearly thrice the UN’s 3% goal). In stay corridors at this time, stablecoin rails are already working at underneath 1%. What we’re just isn’t merely a matter of optimizing the margins, however a structural hole within the fastest-growing areas of the worldwide financial system.

SWIFT was constructed for a selected world: giant banks, giant tickets and main monetary centres. It really works completely for that world. But the provider cost in Nairobi, the remittance from Riyadh to Manila, or the commerce settlement between Almaty and Istanbul has been making do with infrastructure designed for another person’s financial system.

That is the hole stablecoins are shifting into, and so they’re not a product however actual plumbing.

Chart 1: The Remittance Price Hole

Sources: World Financial institution (Q1 2025); UN SDG 10.c; Transak / Operational hall information

What we observe from the bottom

I hung out with regulators and market operators throughout high-growth corridors and a sample that emerges is that individuals closest to the friction are the least ideological concerning the answer. They’re those truly attempting to combine stablecoins into the prevailing monetary system.

In Kigali for instance, the framing is not “crypto adoption.” Rwanda’s Nationwide Financial institution launched a CBDC pilot in February with cross-border interoperability as the specific design precedence. A draft Digital Belongings Legislation now in parliament applies a clear two-tier construction: Central Financial institution oversight for cost stablecoins and Capital Markets Authority for funding devices. A fintech license passporting settlement with Kenya, signed in March, is already being designed as a template for the East African Neighborhood. That is regulatory infrastructure being constructed with precision, for a selected drawback, by individuals who perceive their very own market.

The perception just isn’t Rwanda-specific, however Africa-wide, the place cell cash already features because the default monetary layer. With over a billion registered accounts, 96% monetary inclusion in markets like Rwanda, this distribution infrastructure took many years to construct. What cell cash by no means solved for is cross-border interoperability. Stablecoins match that hole naturally, not changing fiat currencies, however performing because the settlement layer that makes cell cash environment friendly.

The identical logic, 4 corridors

Center East

The Central Financial institution of UAE’s Cost Token Companies Regulation treats stablecoins as settlement infrastructure somewhat than speculative securities. That regulatory framing is sensible and permits banks to subject AED stablecoins that can be utilized straight as a way of cost, and banks and licensed fintechs can construct on stablecoin rails with out treating each transaction as a legal responsibility. On this approach, the Gulf stablecoin settlement is occurring inside regulated perimeters.

CIS markets

In Kazakhstan, Uzbekistan and Georgia, the motive force is greenback entry. Home foreign money volatility creates structural demand for USD, and formal banking does not reliably present them. Stablecoin adoption right here is dollarization leveraging a brand new distribution channel. The institutional alternative is offering that entry inside a compliance framework, with the custody and reserve requirements that make it sturdy.

Southeast Asia

In Southeast Asia, the motive force is value and pace. In corridors like Gulf-Indonesia or Gulf-Philippines for remittances, stablecoin rails remove the necessity for pre-funding and pace up settlement from days to minutes (usually underneath 20 minutes, 24/7). Price reductions of 40–80% are already observable in operational flows.

I engaged with regulators, banks and fintechs in these markets. The query right here is: how can we facilitate greater volumes on stablecoin rails and provides again to the households?

Africa

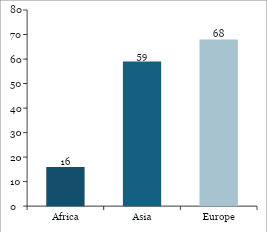

Remittances are costly, however the B2B case is pressing as effectively. Intra-African commerce solely accounts for 16% of whole commerce, in opposition to 68% for Europe and 59% for Asia. The AfCFTA created the authorized structure for a $3.4 trillion market, however the cost infrastructure hasn’t saved up. Chinese language merchants sourcing African items are already settling in USDT as a result of it’s superior for his or her transaction sizes and timelines. To make this correctly institutional and largely adopted, the essence is to ensure that the exercise occurs compliantly, with correct rails.

Chart 2: Intra-Regional Commerce Share — Africa vs Friends

Sources: UNCTAD / AfDB / WTO; World Financial institution / African Union (AfCFTA projection)

Stablecoins are infrastructure

International banks and fintechs are nonetheless largely approaching stablecoins as a product to distribute to prospects. The extra vital alternative is treating them as infrastructure to construct on, notably in remittances and B2B cost flows: treasury administration, provider funds and FX settlement. These are flows the place the pace enchancment and value discount are measurable (minutes vs days, foundation factors), and the place the compliance trails on well-designed digital rails are demonstrable and trackable. These embody on-chain transaction monitoring, pockets attribution and automatic regulatory reporting that produces a compliance report that casual switch channels structurally can not. The information generated by these rails is what will get correspondent banking relationships restored in markets the place de-risking has reduce them.

Fixing the friction

What stays to be solved for the infrastructure to correctly work at scale? Regulatory frameworks that outline reserve requirements and redemption rights, cross-border supervisory coordination and AML/CFT legal guidelines interoperability.

All that is being labored by, and extra available in the market that issues (high-growth) than in established developed international locations.

From expertise working with regulators and now proactively partaking with them, I discovered that the sample that works is: 1. A phased licensing framework that lets regulators be taught alongside the market; 2. Proportionate necessities scaled to institutional dimension and threat profile; 3. Bilateral passporting agreements that make compliance moveable throughout corridors.

The corridors the place this infrastructure is most wanted should not ready for world requirements to reach however are actively constructing. The query for world establishments is whether or not they’re a part of that structure or arriving late to fintech-leading infrastructure.

Headlines of the Week

Francisco Rodrigues

This week’s headlines present structural progress on Wall Avenue’s onchain push, with a market-structure invoice clearing its largest hurdle, JPMorgan extending its tokenization stack, and asset managers tackling the redemption-speed drawback. Solana has in the meantime saved quietly cementing its infrastructure for institutional use.

- Readability Act clears U.S. Senate committee, on its method to a ultimate take a look at in Congress: Chairman Tim Scott secured a 15-9 bipartisan vote with Democrats Gallego and Alsobrooks crossing over, although unresolved legislation enforcement and government-ethics provisions nonetheless stand between the invoice and a ground vote earlier than the summer season recess.

- JPMorgan recordsdata to launch new tokenized fund as Wall Avenue tokenization race heats up: The Ethereum-based JLTXX fund, run by JPMorgan’s Kinexys blockchain unit, is structured to fulfill GENIUS Act stablecoin reserve necessities — touchdown days after BlackRock filed for its personal tokenized Treasury car.

- BlackRock, Janus Henderson tokenized funds get on the spot redemptions with new $1 billion facility: Grove’s Basin facility advances stablecoin liquidity in opposition to authorised redemptions from BlackRock’s $2.2 billion BUIDL and Janus Henderson’s $1.1 billion JTRSY, concentrating on the multi-day settlement hole that has held again the $15 billion tokenized Treasury market.

- Mike Novogratz’s Galaxy receives New York BitLicense for institutional crypto push: NYDFS cleared GalaxyOne Prime NY to serve hedge funds, RIAs and household places of work on a $9 billion platform, making Galaxy solely the second agency to win a BitLicense in 2026 after Strike.

- Solana is shedding its memecoin popularity as huge banks transfer billions into its ecosystem: A Messari report exhibits Solana’s tokenized RWA market cap jumped 43% QoQ to $2.01 billion, with BlackRock’s BUIDL, Ondo, Franklin Templeton and a Citigroup-PwC commerce finance PoC stay on the community, alongside funds integrations from Visa, Stripe, PayPal and Western Union.

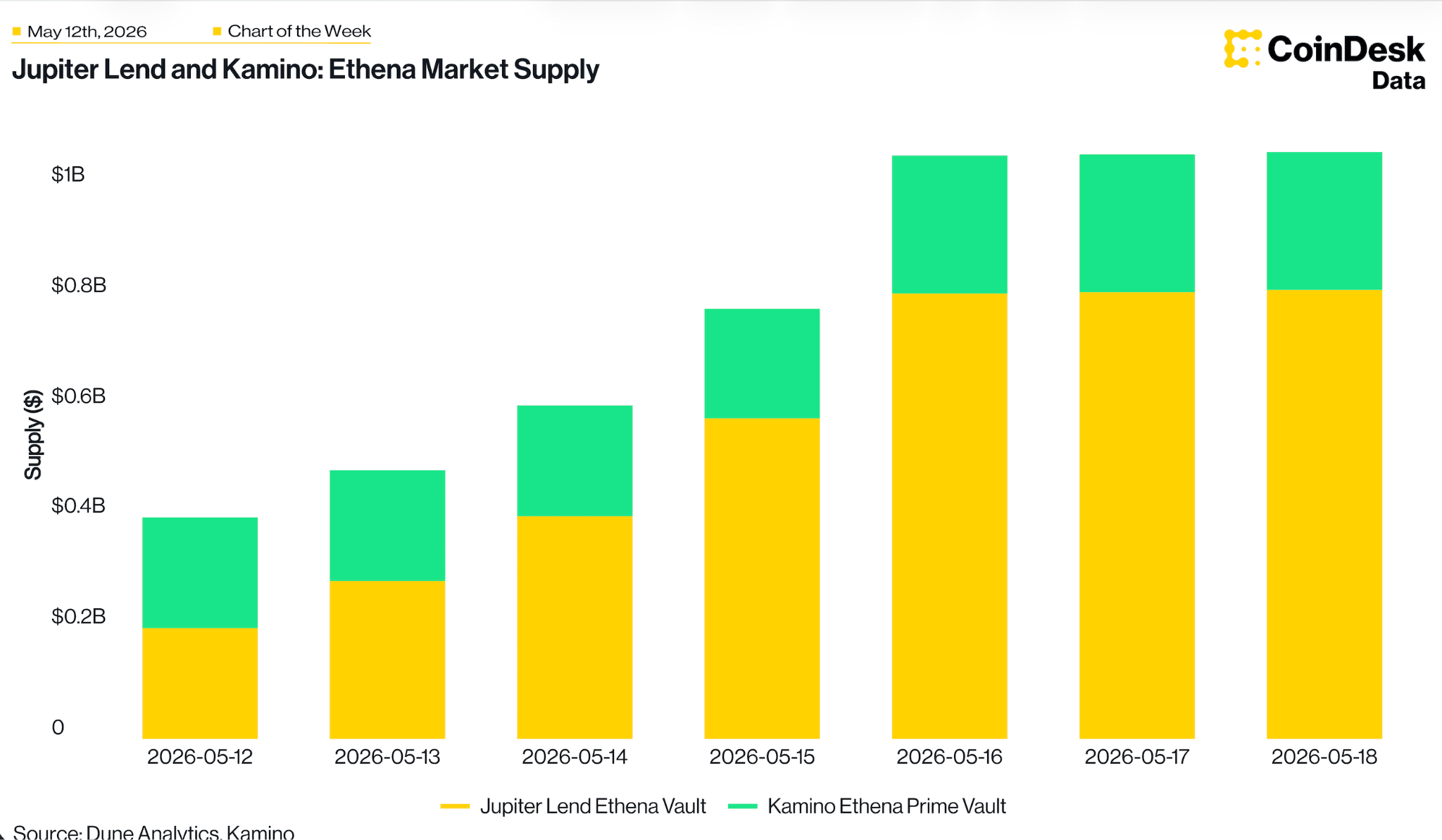

Chart of the Week

Ethena’s Solana lending markets cross $1B in 4 days

Mixed USDe and USDG provide throughout the Bitwise-curated Jupiter Lend market and the Kamino Ethena market rose from $401M on launch day (Could 12) to $1.06B on Could 16 – pushed nearly fully by looper-led progress on Jupiter Lend, the place provide climbed from $201M to $812M whereas Kamino’s Ethena Prime vault held regular round $250M.

Hear. Learn. Watch. Interact.

- Hear: Did you hear? CoinDesk’s Could 2026 Change Benchmark report from CoinDesk Analysis was launched final week. The requirements have been raised and our analysis staff breaks down the rankings.

- Learn: In Crypto for Advisors, Sam Boboev, Founder & CEO at Fintech Wrap Up explains how stablecoins have gotten the cost rails within the digital financial system.

- Watch: Movies are stay from Consensus 2026 by CoinDesk. Rewatch a favourite world thought chief onstage or look ahead to the primary time!

- Interact: CoinDesk will probably be on the Girls in Digital Belongings Discussion board (WIDAF) in NYC on June 3. Let’s join onsite!

On the lookout for extra? Obtain the most recent crypto information from coindesk.com and market updates from coindesk.com/establishments.