Technique (previously often called MicroStrategy) is discovering that strengthening one a part of its more and more advanced steadiness sheet can expose weaknesses elsewhere.

The Bitcoin treasury firm spent $1.5 billion in Might repurchasing convertible notes, decreasing its debt but additionally draining money that buyers considered as a backstop for its preferred-stock dividends. Weeks later, its Variable Charge Collection A Perpetual Stretch Most popular Inventory, often called STRC, fell to a file low of $82.50, or 17.5% beneath its $100 acknowledged worth.

Technique has since began rebuilding the reserve by promoting frequent shares. Nevertheless, the response has sharpened a battle on the middle of Michael Saylor’s financing mannequin: cash retained to assist STRC can’t concurrently be spent shopping for Bitcoin, whereas elevating that money via MSTR gross sales dilutes present frequent shareholders.

CryptoQuant mentioned the stress has change into extreme sufficient that the Saylor-led agency ought to droop Bitcoin purchases till it restores its money reserves and dividend protection. Benchmark Fairness Analysis, in contrast, views STRC’s decline as a market-driven repricing of the yield buyers demand reasonably than proof that the construction is failing.

The disagreement marks the clearest pressure but on Saylor’s effort to remodel Technique from a software program firm into an issuer of Bitcoin-backed “digital credit score.”

Dividend prices outrun the money reserve

STRC was launched in July 2025 as a perpetual most well-liked safety designed to commerce close to $100. Technique can modify its dividend price month-to-month to make the shares extra engaging after they fall beneath that degree.

The safety has since change into an essential supply of funding for Technique’s Bitcoin purchases. That enlargement, nevertheless, has created a quickly rising recurring obligation.

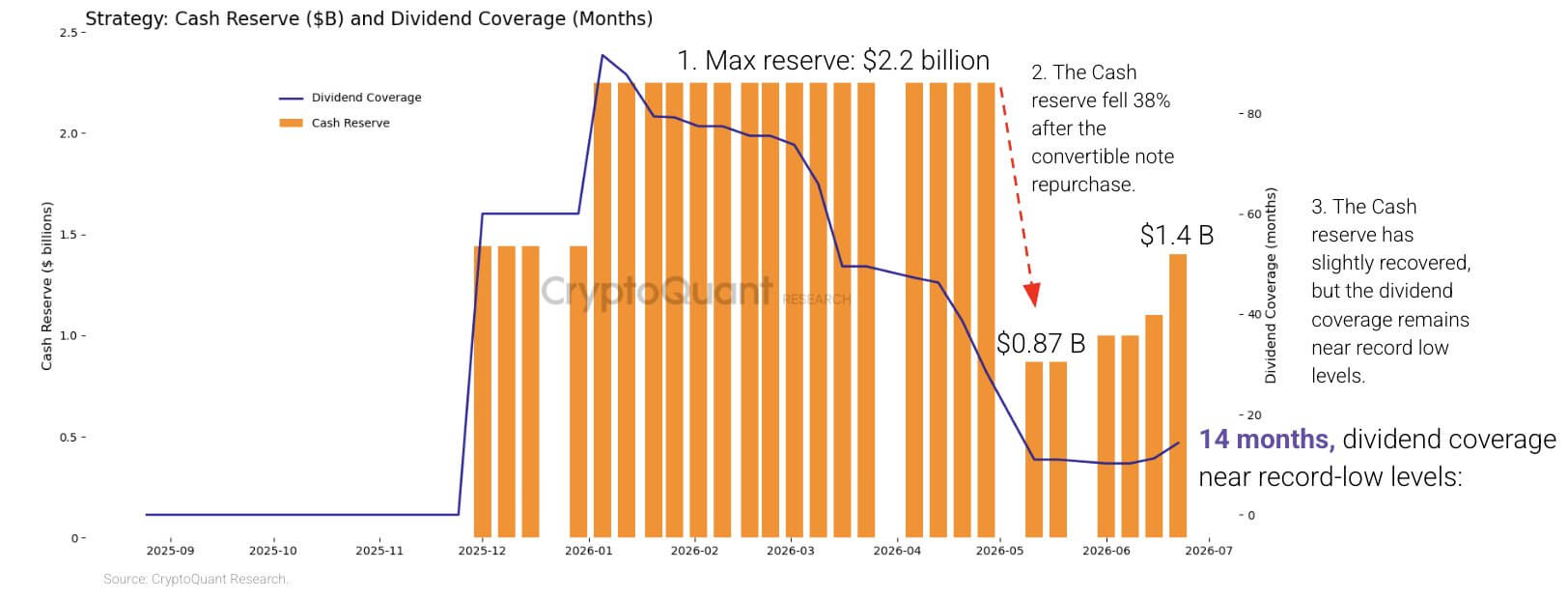

CryptoQuant estimated that Technique’s annualized preferred-dividend obligations have almost quadrupled from about $300 million at the beginning of 2026 to $1.2 billion.

On the identical time, the corporate’s money reserves declined by 38% from the start of the 12 months, with the sharpest discount following the Might repurchase of its 0% convertible notes due in 2029.

Whereas retiring the notes eliminated a future declare from the steadiness sheet, it additionally decreased the pool of liquid funds out there to cowl dividends throughout a interval when Bitcoin costs and Technique’s securities had been below stress.

CryptoQuant mentioned the corporate entered 2026 with sufficient money to cowl greater than seven years of dividends. The agency estimated that protection had fallen to about 14 months after Technique rebuilt its money place to $1.4 billion.

The analytics firm estimated that Technique would want about $2.8 billion to revive a 24-month reserve.

STRC permits Technique to defer its dividends, however the funds are cumulative, that means skipped distributions stay payable. A suspension might quickly protect money whereas undermining investor confidence and making future preferred-stock issuance costlier.

Technique, due to this fact, has few painless choices. Elevating STRC’s dividend might assist demand however would enhance its money burden. Retaining extra capital would sluggish Bitcoin purchases, whereas further MSTR gross sales would switch extra of the associated fee to frequent shareholders via dilution.

In the meantime, Technique’s Bitcoin treasury gives one other potential supply of liquidity, however utilizing it now would additionally come at a price.

CryptoQuant estimated that the holdings carried an unrealized lack of about $10.6 billion at prevailing costs. Promoting throughout the downturn would crystallize a few of these losses and problem the corporate’s longstanding accumulation narrative.

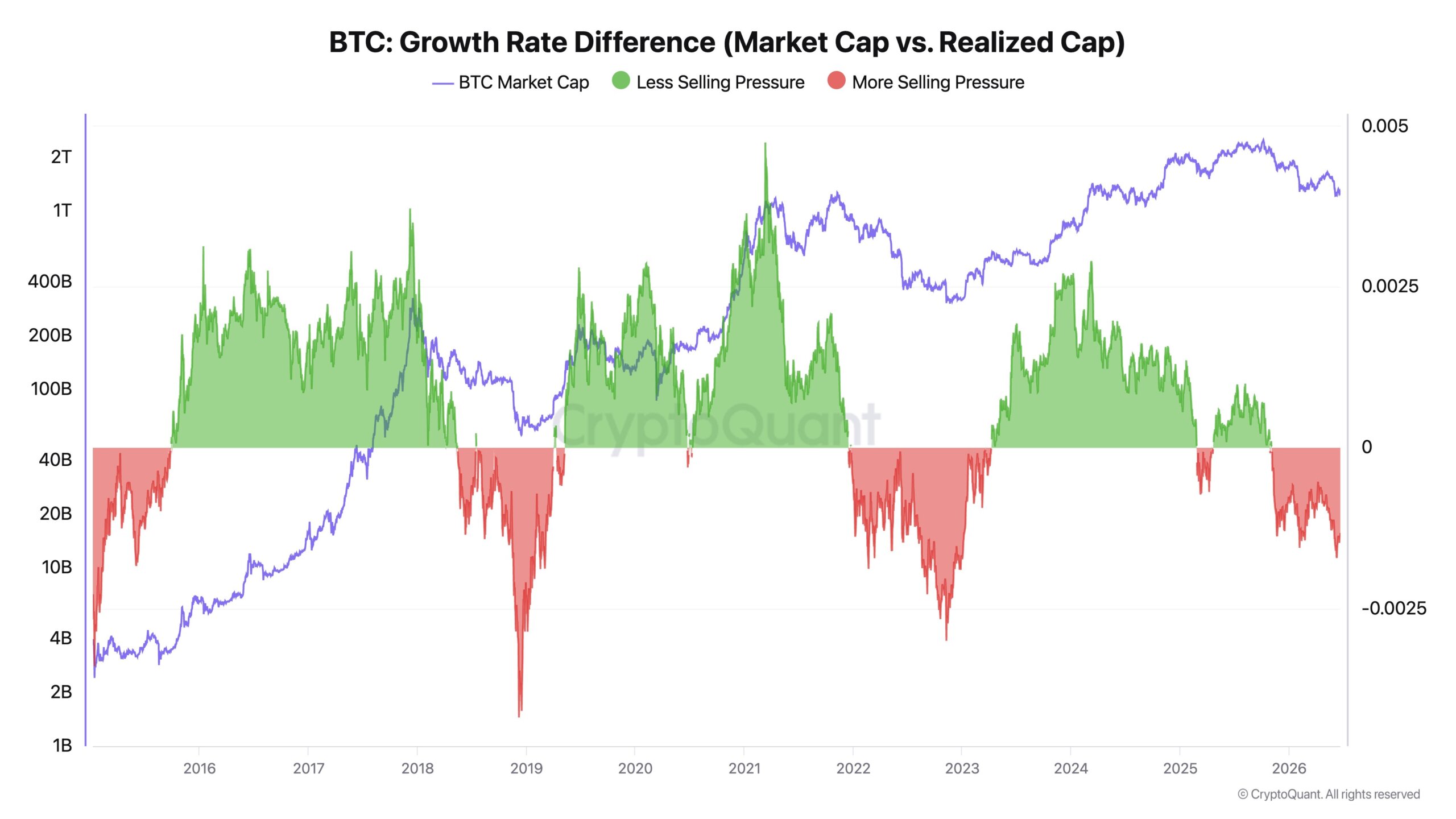

CryptoQuant Chief Govt Ki Younger Ju mentioned Technique’s latest Bitcoin purchases seemed to be absorbing capital with out producing a sustained enhance within the cryptocurrency’s value.

He described the shopping for as extra of a “liquidity sink” than a value catalyst and mentioned the corporate ought to prioritize money protection earlier than making additional acquisitions.

Ju famous that Bitcoin’s realized capitalization had elevated by $467 billion over the earlier two years, at the same time as its value declined by about 1%. He argued that the divergence confirmed contemporary capital was largely permitting cash to vary palms reasonably than driving a broad revaluation of the market.

Below situations of restricted promoting, giant institutional purchases can transfer costs sharply, Ju mentioned. When promoting stress is elevated, the identical demand could do little greater than assist an present buying and selling vary.

He urged Technique to interchange its follow of shopping for each time capital turns into out there with a model-driven acquisition framework. He additionally known as for guidelines that will enable the corporate to promote parts of its holdings throughout future market peaks, arguing that restricted gross sales might cut back leverage, notice worth for shareholders, and unencumber capital for purchases throughout later downturns.

Such an method would signify a pointy departure from Saylor’s public dedication to persistent Bitcoin accumulation.

Widespread shareholders change into the backstop

In the meantime, Technique’s newest fundraising confirmed which possibility administration is presently ready to make use of.

The corporate offered about 2.7 million MSTR shares final week, elevating $335.5 million. It directed $300 million, or nearly 90% of the proceeds, to its money reserve and used the remaining $35 million to purchase 520 Bitcoin at a median value of $67,068.

The allocation confirmed that rebuilding liquidity had quickly taken precedence over maximizing Bitcoin purchases. Technique nonetheless expanded its holdings to 847,363 Bitcoin, bought for about $64.01 billion at a median value of $75,651.

The money injection additionally got here with a bigger share rely. Technique’s diluted shares elevated to about 388.6 million from 386.1 million per week earlier. Its year-to-date BTC Yield, an organization metric measuring modifications in Bitcoin holdings relative to assumed diluted shares, fell to 11.8% from 13% 4 weeks earlier.

The decline doesn’t imply Technique owns much less Bitcoin. It reveals that Bitcoin holdings per assumed diluted share are growing extra slowly as the corporate points further fairness.

That dynamic might change into extra pronounced if STRC stays considerably beneath $100. Issuing extra most well-liked shares at unfavorable costs would change into more durable or require larger payouts, leaving frequent fairness as Technique’s most available supply of capital.

MSTR shareholders would then be financing each the corporate’s Bitcoin purchases and the money reserve supporting securities with senior claims on the steadiness sheet.

Supporters of Technique’s mannequin dispute the conclusion that its common-stock gross sales have weakened buyers’ financial place.

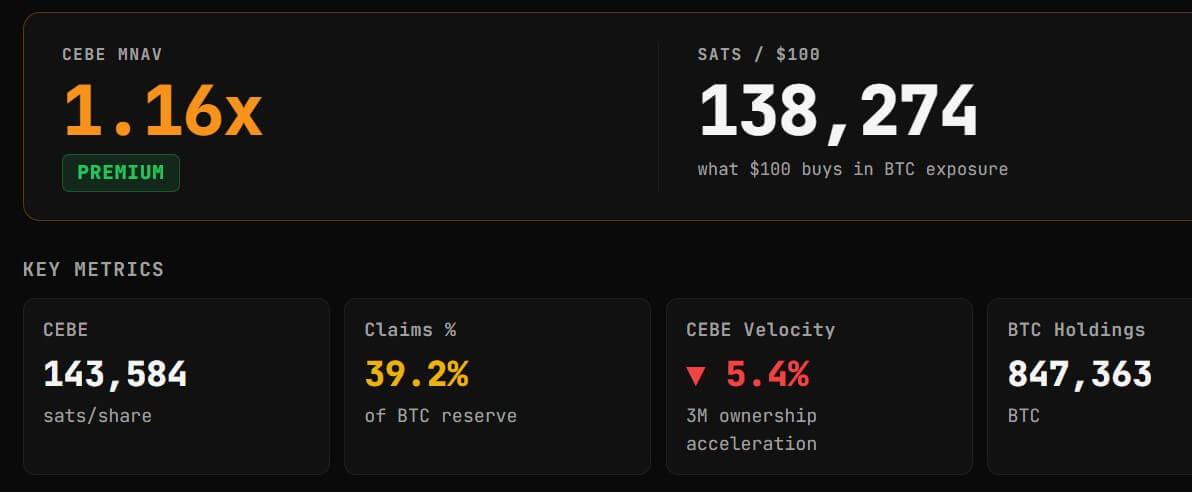

Adam Livingston, a pro-Technique analyst, mentioned the corporate added about 24,029 satoshis of Widespread Fairness Bitcoin Publicity per fundamental share throughout the 12 months regardless of issuing further inventory.

Widespread Fairness Bitcoin Publicity, or CEBE, makes an attempt to calculate the Bitcoin attributable to frequent shareholders after deducting debt, most well-liked inventory, and different senior obligations. Livingston argued that Technique used the proceeds from new shares to amass sufficient Bitcoin to extend the web publicity supporting every fundamental share.

That doesn’t imply the issuance was not dilutive. Present shareholders nonetheless personal a smaller share of the corporate after new inventory is offered. Livingston’s argument is as an alternative that the property attributable to every share rose by sufficient to offset the rise within the share rely.

Livingston’s conclusion additionally differs from the decline in Technique’s reported BTC Yield as a result of the 2 measures use totally different methodologies. Technique’s metric depends on assumed diluted shares, whereas Livingston’s calculation makes use of fundamental shares and adjusts Bitcoin holdings for senior claims.

Knowledge from CEBE Tracker positioned Technique’s CEBE a number of to web asset worth at about 1.15 occasions, that means MSTR continued to commerce at a premium to the estimated web Bitcoin publicity attributable to frequent holders.

That premium stays central to Technique’s mannequin. So long as the corporate can difficulty inventory above the worth of the Bitcoin backing every frequent share and use the proceeds accretively, advocates argue that new issuance can enhance reasonably than destroy per-share publicity.

The danger is that the premium narrows whereas money necessities and most well-liked obligations proceed to rise. Below these situations, Technique might nonetheless increase capital, however every transaction would generate much less incremental worth for present frequent shareholders.

In the meantime, this market stress has impacted MSTR’s value efficiency. Yahoo Finance information reveals MSTR has fallen beneath the $100 mark, its lowest value degree since March 2024.

Buyers disagree over whether or not the mannequin is breaking

CryptoQuant views STRC’s low cost as proof that Technique’s liquid assets have did not preserve tempo with its obligations. Benchmark analyst Mark Palmer sees the identical decline as a standard adjustment within the yield buyers require.

Palmer rejected comparisons between STRC and failed stablecoins reminiscent of TerraUSD, noting that STRC is a perpetual most well-liked inventory reasonably than an asset supported by an algorithmic peg. Technique has mentioned it intends to handle STRC close to $100 however has not assured that value.

At about $87, a dividend calculated at roughly 11.5% of the $100 acknowledged worth offers consumers a market yield of greater than 13%. That means buyers are demanding better compensation for Technique’s Bitcoin publicity, money necessities and more and more advanced capital construction.

Benchmark maintained its purchase ranking on MSTR and a $570 value goal, arguing that elevated STRC buying and selling volumes confirmed energetic repricing reasonably than structural deterioration. The agency additionally pointed to Technique’s Bitcoin treasury, value roughly $55 billion on the costs utilized in its evaluation, and the corporate’s continued capacity to regulate dividends and lift capital.

Charles Edwards, founding father of Capriole Investments, provided a extra extreme evaluation. He mentioned a enterprise mannequin depending on continued Bitcoin appreciation to assist dividends and yield merchandise would ultimately change into unsustainable.

He famous:

“So long as his enterprise mannequin requires Bitcoin ‘quantity go up’ to outlive and pay yield or dividends, it’s a ticking time bomb. Perhaps not this cycle, however the music will cease.”

Edwards argued that Technique ought to cut back its liabilities, unwind its yield merchandise, and return to holding a much less encumbered Bitcoin place. He additionally proposed buying digital-asset treasury corporations buying and selling at giant reductions to their web asset values and ultimately constructing working companies round Bitcoin lending, borrowing, and settlement.

These proposals would contain important obstacles. Repaying Technique’s liabilities might require promoting Bitcoin, issuing extra fairness, or each. A transfer into lending would additionally introduce regulatory, credit score, and counterparty dangers past these of a treasury firm holding Bitcoin on its steadiness sheet.

Nonetheless, Edwards’ criticism captures the longer-term query going through the corporate: whether or not Technique can proceed increasing its capital construction with out turning into more and more depending on larger Bitcoin costs and uninterrupted entry to fairness markets.

The competing assessments are usually not completely incompatible. Technique could maintain enough property to satisfy its obligations over the long run, even because it faces a near-term scarcity of low cost, liquid capital.

Its newest fundraising choice displays that distinction. Technique might nonetheless entry the common-stock market, nevertheless it needed to direct many of the proceeds to rebuilding money reasonably than accelerating Bitcoin purchases.

That trade-off is more likely to outline the subsequent part of Saylor’s experiment. Elevating the STRC dividend would enhance prices. Promoting extra MSTR would dilute shareholders. Promoting Bitcoin might lock in losses. Suspending funds might undermine confidence in Technique’s preferred-stock franchise.

For now, the corporate is selecting money and dilution and asking frequent shareholders to soak up the price of preserving its Bitcoin funding machine intact.