BlackRock’s 1% to 2% Bitcoin allocation vary reads as a bullish nod to advisor adoption, however it additionally works as a boundary. As soon as Bitcoin is included in a mannequin portfolio, its upside runs by way of rebalancing bands, tax location, and generally a mortgage that retains the place intact.

BlackRock Funding Institute frames 1% to 2% as an inexpensive multi-asset vary, supplied the investor believes in continued adoption and might abdomen sharp drops.

The agency sizes the place primarily based on its contribution to general portfolio danger, and that danger climbs shortly in an ordinary 60/40 combine. A 1% Bitcoin allocation provides roughly 2% to whole portfolio danger, a 2% allocation provides roughly 5%, and a 4% allocation provides roughly 14%.

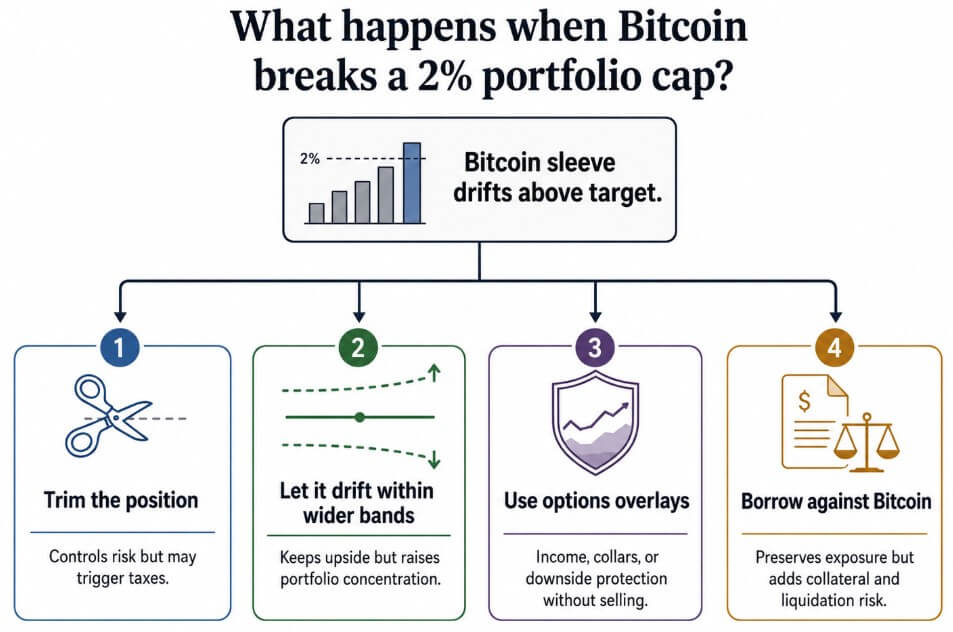

That danger math turns the ceiling right into a reside determination level. If Bitcoin outruns shares and bonds throughout the mannequin, an advisor can trim it, let it drift, hedge it, or transfer publicity elsewhere.

A 2% Bitcoin sleeve wants roughly a 51.5% achieve, with the remainder of the portfolio flat, to float to three%. It wants roughly a 104% achieve to float to 4%, the purpose at which resetting the place to 2% would imply promoting virtually half the sleeve.

| BTC allocation / drift level | Portfolio affect | What it forces advisors to determine |

|---|---|---|

| 1% BTC allocation | ~2% of whole portfolio danger | Sufficiently small to suit inside a conventional danger finances |

| 2% BTC allocation | ~5% of whole portfolio danger | BlackRock’s higher vary; turns into the important thing administration ceiling |

| 4% BTC allocation | ~14% of whole portfolio danger | Bitcoin begins dominating danger contribution |

| 2% sleeve after ~51.5% BTC rally | Drifts to ~3% | Advisor should determine whether or not to trim, hedge, or let it run |

| 2% sleeve after ~104% BTC rally | Drifts to ~4% | Resetting to 2% means promoting about half the BTC sleeve |

BlackRock’s IBIT alone had almost $60 billion in internet flows as of July 2, a dimension at which portfolio administration decisions begin to matter for the broader market.

Citi reduce its 12-month Bitcoin value goal to $82,000 from $112,000 on July 1 and dropped its influx assumption to zero from $10 billion.

The agency pointed to Bitcoin ETF flows working damaging year-to-date, and Farside Buyers’ knowledge confirmed that US-traded spot Bitcoin ETFs misplaced over $2.7 billion throughout 10 buying and selling days from late June to July 1.

Why promoting hurts

For a long-time Bitcoin holder, promoting to remain beneath a cap can really feel like giving up the mistaken asset.

Mauricio Di Bartolomeo, co-founder and chief technique officer of the Bitcoin lending agency Ledn, sees a variety of debtors.

They embrace private and non-private corporations working on a Bitcoin commonplace, in addition to households in Latin America working round economies. {Couples} additionally borrow towards Bitcoin to purchase their first dwelling.

He instructed mycryptopot that “debtors are available all sizes and shapes,” and what connects them is a choice for financing over a sale, retaining the asset they contemplate their strongest holding.

Taxes play an element in that call, however Di Bartolomeo says the mathematics holds up by itself, taxes apart. He factors to a borrower who took a Bitcoin-backed mortgage in January 2020 and managed it responsibly.

Even internet of curiosity and costs, that individual would sit in a stronger monetary place in the present day than somebody who offered Bitcoin outright that very same month.

Di Bartolomeo estimated that debtors utilizing Bitcoin as collateral ought to put aside at the very least 100% of that collateral’s worth to deal with market volatility. As soon as somebody borrows towards over half of a Bitcoin portfolio, the cushion defending them from a pointy drawdown will get skinny.

The case towards pressured promoting

Kelly Ye, co-founder and chief funding officer of CoinBridge, pushed again on the belief that mannequin portfolios already drive Bitcoin ETF flows.

She pointed to Morgan Stanley’s figures, noting that roughly 80% of Bitcoin ETF exercise on the agency’s platform stays self-directed, with about 20% routed by way of advisors.

Massive wirehouses sometimes require six to 12 months of efficiency historical past, operational due diligence, and compliance assessment. She mentioned that solely then does a brand new ETF earn a spot in a centralized mannequin.

That timeline retains most of in the present day’s Bitcoin publicity within the arms of particular person buyers making their very own choices.

Even as soon as advisors undertake Bitcoin, Ye expects a broader toolkit to deal with a lot of the work, with a sale as a final resort. Rebalancing bands could be set wider for a unstable asset than for bonds or large-cap shares.

Advisors can rebalance utilizing new shopper contributions, trim solely a portion of a place, or place the Bitcoin sleeve in an IRA or a Roth account. A sale inside a kind of accounts avoids an instantaneous tax invoice.

Many present ETF holders are nonetheless close to their entry value, Ye notes. Glassnode places the common ETF holder’s price foundation close to $83,000, effectively above Bitcoin’s value by way of the again half of the second quarter.

Which means a big share of holders would present a loss in the event that they offered in the present day.

The choices market backs her up, as IBIT choices quantity now rivals native Bitcoin choices markets.

OCC reported 689.5 million ETF choices contracts traded in June, up 69.7% from a 12 months earlier. Kaiko and MerQube knowledge cited by ETF Specific present IBIT choices open curiosity peaked at $53.3 billion in its first 12 months.

Goldman Sachs has filed for a Bitcoin ETF constructed to pair Bitcoin publicity with earnings from choices trades, becoming a member of a set of instruments constructed virtually totally for the reason that ETF’s 2024 launch.

Letting the winner run

If the toolkit does the work, Bitcoin’s rally retains compounding inside advisors’ books, and gross sales keep occasional. Wider tolerance bands take up the early drift, and new shopper money flows nudge portfolios again towards goal on their very own.

Retirement accounts maintain a bigger share of the Bitcoin sleeve over time, decreasing the tax invoice at every rebalance.

Choices overlays cowl the remainder, letting advisors accumulate earnings or purchase safety whereas retaining the underlying place intact. On this model, Wall Avenue financializes Bitcoin, and the place continues to compound.

Trimming on schedule

The choice path runs by way of tighter mechanics. If giant platforms construct Bitcoin into fashions utilizing the identical slender bands they apply to shares and bonds, a rally triggers a trim quick.

Bitwise says belongings monitoring third-party mannequin portfolios grew from $400 billion in 2023 to over $645 billion in 2025, a 62% leap.

Because the model-portfolio infrastructure grows, a 2% Bitcoin sleeve turns into a recurring supply of provide each time Bitcoin rallies exhausting, and a profitable place turns into a scheduled sale.

If Bitcoin-backed borrowing grows on the similar tempo with much less self-discipline, a pointy drawdown might add pressured liquidations on prime of the trims.

| Situation | What occurs | Market implication |

|---|---|---|

| Managed drift | Advisors permit Bitcoin to maneuver above 2% inside wider tolerance bands | Restricted pressured promoting; Bitcoin compounds inside portfolios |

| Tax-aware adoption | Extra BTC ETF publicity strikes into IRAs, Roth accounts, and retirement plans | Rebalancing turns into much less tax-sensitive |

| Choices-led administration | Advisors use coated calls, collars, or draw back places as a substitute of promoting spot publicity | Volatility is managed with out totally decreasing BTC publicity |

| Mechanical trimming | Mannequin portfolios apply slender bands and promote as soon as BTC runs above goal | Bitcoin rallies create recurring provide from advisors |

| Collateral stress | Debtors overuse Bitcoin-backed loans and BTC sells off sharply | Liquidations amplify draw back moderately than avoiding gross sales |

Bitcoin is the asset that was as soon as outlined by hold-forever conviction and is now turning into a managed sleeve, with guidelines for rebalancing, tax location, and when a mortgage replaces a sale.

Administration is the open combat that runs by way of rebalancing bands, tax location, and, for some holders, a mortgage that retains the Bitcoin the place it’s.