A deep dive into Hut 8 Mining, uncovering its usually neglected enterprise sectors. Perceive its monetary efficiency, strategic initiatives and HPC/AI developments.

The next visitor publish comes from Bitcoinminingstock.io, offering complete information, in-depth analysis, and analyses on Bitcoin mining shares. Initially printed on Nov. 29, 2024, it was penned by Bitcoinminingstock.io writer Cindy Feng.

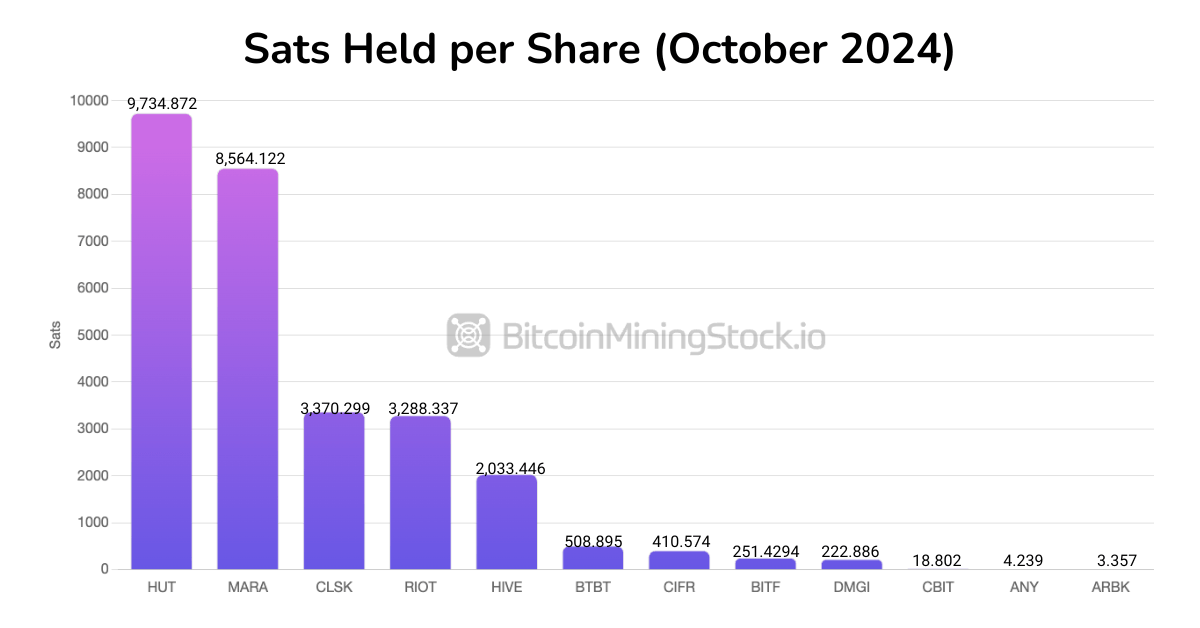

The YTD efficiency of Hut 8 Mining Corp. (NASDAQ: HUT) has made it a standout. Different metrics like Satoshi per share are additionally eye-catching, the place Hut 8 outperforms MARA and the place the latter is the biggest Bitcoin holder amongst all public Bitcoin mining corporations. As one of many first Bitcoin miners to go public (initially listed on the TSX in 2018 and in a while Nasdaq in 2021) Hut 8 has skilled the complete spectrum of market cycles. By analyzing this Bitcoin mining veteran, we will achieve useful insights to raised navigate the ever evolving business.

Supply: https://bitcoinminingstock.io/holdings

Primary Profile

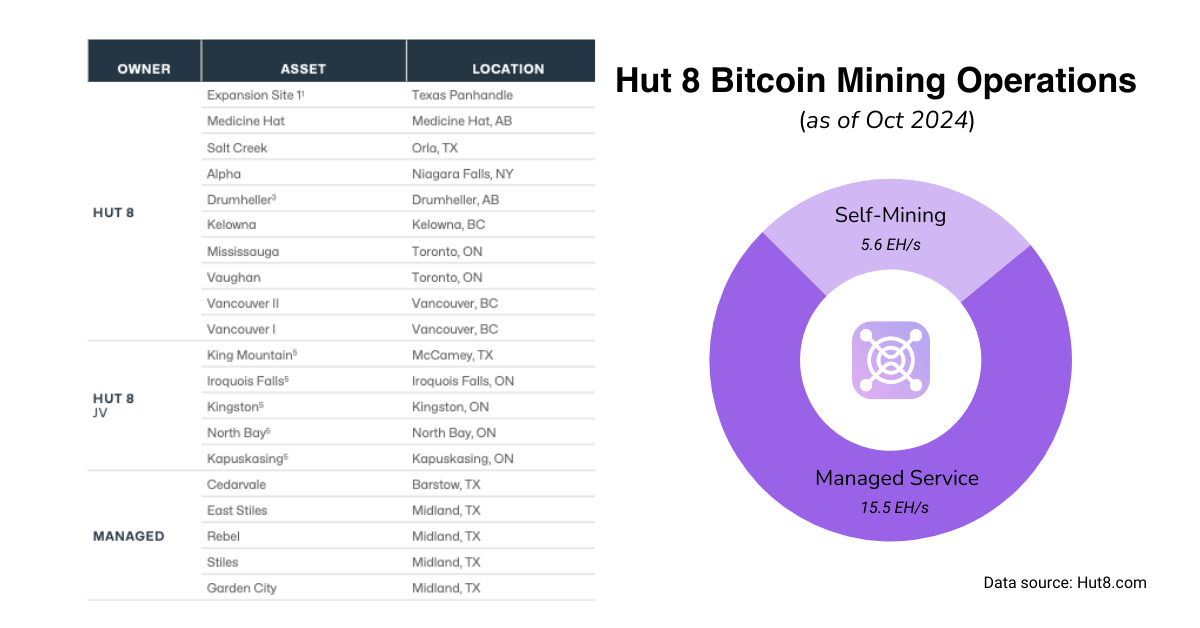

Hut 8 is a Bitcoin miner with operations in Canada and the USA. The corporate at the moment has 20 websites in its portfolio, comprising each operational amenities and others at the moment underneath growth. On the time of writing, Hut 8 reported a mixed capability of 967 MW, equal to 20.1 EH/s. This consists of 5.6 EH/s for self-mining, and the remaining allotted to managed providers.

Past its core mining operations, Hut 8 engages in Bitcoin mining tools gross sales and repairs. Moreover, the corporate’s Far North JV website participates in grid balancing applications by pure gasoline energy crops in Ontario, Canada.

In July, Hut 8 introduced the closing of a $150M funding from Coatue, after which launched GPU-as-a-Service in September. It’s clear that the corporate is accelerating its place within the HPC/AI sector. In latest advertising supplies, Hut 8 describes itself as an “power infrastructure platform”, which additionally alerts a gradual transfer away from Bitcoin mining as its sole focus.

Q3 Efficiency

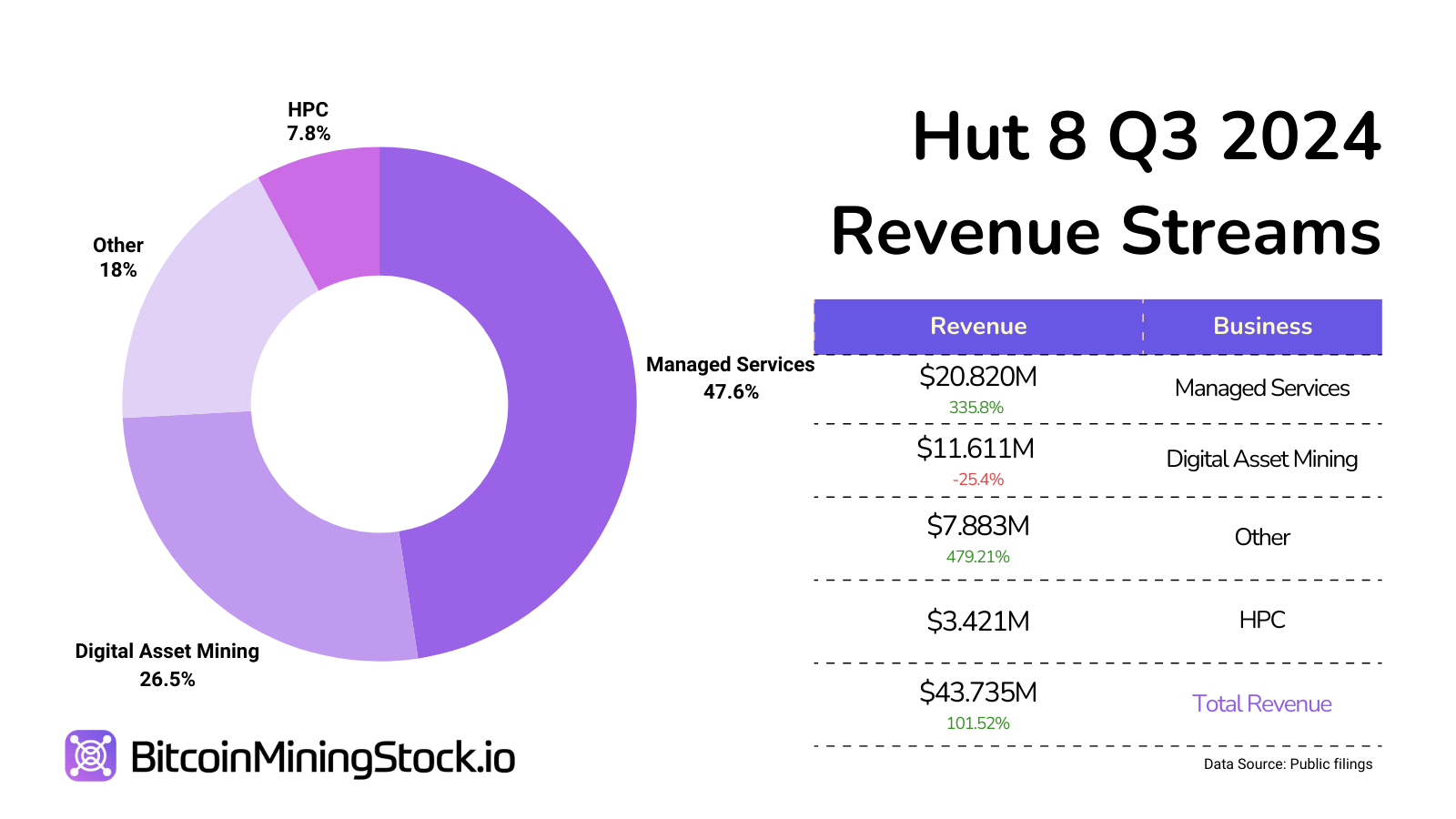

In Q3 2024, Hut 8 demonstrated sturdy income progress and strategic execution pushed by diversification into HPC and energy-efficient mining.

Whole income for Q3 2024 rose considerably to $43.7M, a 101% improve in comparison with the identical interval final 12 months (24% QoQ improve). This progress was fuelled by managed providers income, which surged 336% to $20.8M, and HPC providers contributing $3.4M. Digital asset mining income nonetheless fell by 25% to $11.6M, reflecting the influence of elevated Bitcoin community problem and the April 2024 halving occasion.

Web earnings turned optimistic at $0.9M in comparison with a $4.4M loss in Q3 2023. Nonetheless adjusted EBITDA fell to $5.6M, a 51% lower, pushed largely by a pointy rise in working bills. Notably, stock-based compensation alone accounted for $4.96M, a 1536% YoY improve.

On the operational entrance, Hut 8’s effectivity efforts resulted in a 33% YoY discount in power prices to $0.029 per kWh. Nonetheless Bitcoin mining prices elevated to $31,482 per BTC when contemplating power prices alone, indicating areas that require additional optimization to take care of profitability.

Managed Companies: Steady Recurring Income

Managed providers, although usually neglected by analysts, accounted for practically half of Hut 8’s whole income in Q3 and exhibited the biggest YoY progress amongst all enterprise segments. These providers contain complete mission administration for purchasers’ information facilities together with design, development, and ongoing operation, tailor-made to the shoppers’ particular wants. Ruled by long-term Undertaking Administration Agreements (PMAs) that usually span 4 to 10 years with potential renewal choices, these providers present a steady income stream.

The income from managed providers is derived from a mixture of mounted month-to-month charges, variable reimbursements, and sometimes equity-based compensation. In Q3, administration charges elevated to $4.1M from $3.4M in the identical interval final 12 months, whereas price reimbursements rose to $1.9M from $1.4M. Moreover, the corporate acquired $1.3M in buyer fairness and a one-time termination charge of $13.5M from MARA associated to the termination of PMAs for the Kearney and Granbury websites.

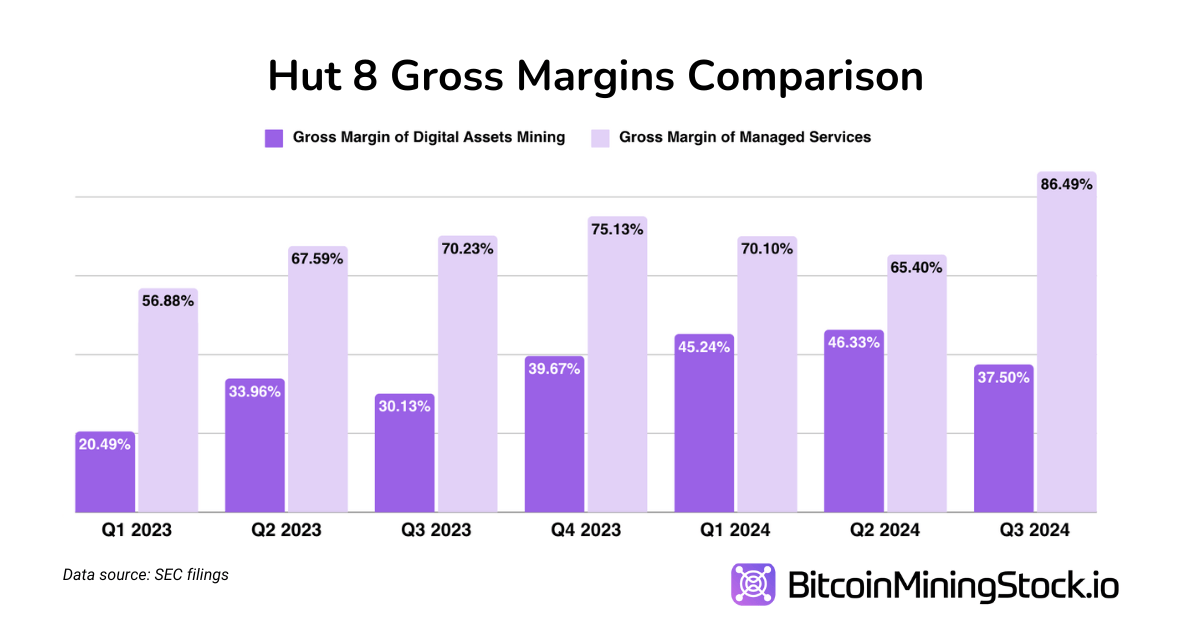

Excluding one-off revenues, the recurring earnings from managed providersstands at roughly $6M per quarter. To not point out its round 70% of the gross margin fee. This will clarify why Hut 8 allocates practically half of its whole hashrate to managed providers. It additionally validates Hut 8’s experience in information heart operations and makes the brand new model as an “power infrastructure platform” extra convincing.

For Hut 8, the gross margins of managed providers are larger than these of Bitcoin mining, and this stays constant even after the Bitcoin Halving.

AI and HPC Ventures: Diversification with Strategic Backing

Hut 8’s HPC/AI income solely elevated by 1.66% in comparison with final quarter, however the progress potential of this phase seems promising. In July the corporate secured a $150M funding from Coatue Administration, a famend technology-focused funding agency with over $47B in belongings underneath administration. Coatue is thought for its strategic investments in GPU infrastructure and AI information facilities, having backed high-profile corporations comparable to Tesla, ByteDance, and Stripe.

Hut 8 Joins Coatue’s AI Portfolio (screenshot from its presentation deck)

This partnership offers Hut 8 with essential capital for deploying and scaling AI and HPC infrastructure, together with NVIDIA H100 GPUs in its GPU-as-a-Service vertical. Furthermore, it grants entry to Coatue’s community of technological experience and market insights, enhancing Hut 8’s credibility and market place within the AI and HPC sectors.

The success of this enterprise depends upon Hut 8’s capacity to seize market share in a aggressive panorama dominated by established HPC suppliers. Regardless, Coatue’s backing alerts confidence in Hut 8’s technique, infrastructure, and execution functionality.

P.S. Hut 8’s HPC providers primarily embody colocation and cloud options. To know technical elements, you might discover this text from Digital Mining Answer useful.

Strategic Initiatives: ASIC Fleet Improve and BITMAIN Partnership

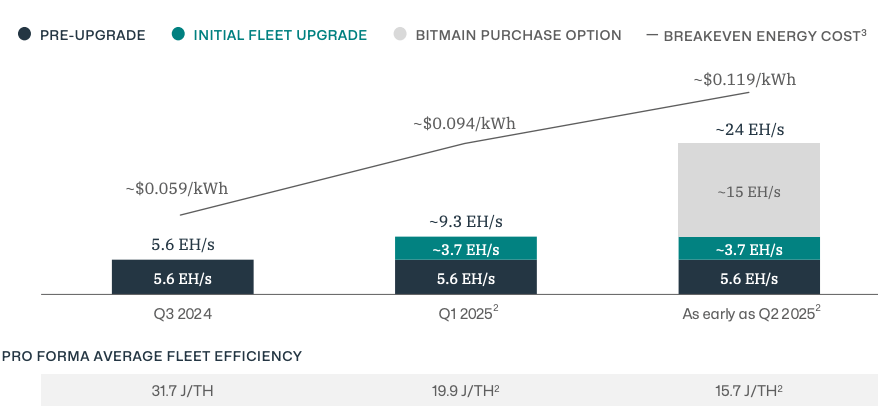

Hut 8 has undertaken important strategic initiatives to boost its mining capabilities and operational effectivity. In early November, the corporate introduced an ASIC fleet improve with the preliminary buy of 31,145 BITMAIN Antminer S21+ miners, scheduled for deployment in early 2025. This improve is anticipated to spice up Hut 8’s self-mining hashrate by roughly 3.7 EH/s to a complete of 9.3 EH/s, representing a 66% improve. This may enhance power effectivity by decreasing consumption by 37%, reaching an effectivity fee of 19.9 J/TH.

Hut 8 Fleet Improve Abstract (screenshot from its Q3 Outcomes Deck)

Earlier in September, Hut 8 entered right into a 15 EH/s colocation settlement with BITMAIN at their Vega website, anticipating the deployment of next-generation U3S21EXPH miners in Q2 2025. To completely leverage liquid-to-chip cooling expertise, Hut 8 has developed a customized design for its Bitcoin mining information heart infrastructure. Their settlement features a buy choice, enabling Hut 8 to probably scale its self-mining hashrate to round 24 EH/s by mid-2025.

Capital Construction and Liquidity

As of Q3 2024, Hut 8 had $72.3M in money and digital asset holdings valued at $576.5M. The corporate’s conversion of a $37.9M mortgage with Anchorage Digitalinto fairness improved its steadiness sheet by eliminating future curiosity obligations of roughly $17M over three years.

Regardless of this, Hut 8’s stock-based compensation rose considerably in 2024 (for the 9 months ending September 30) after reaching $16.4M—an 895.8% YoY improve in comparison with the identical interval final 12 months. Moreover, the corporate’s reliance on Bitcoin gross sales for liquidity ties its operational funding to market circumstances, exposing it to potential money move volatility throughout bearish cycles.

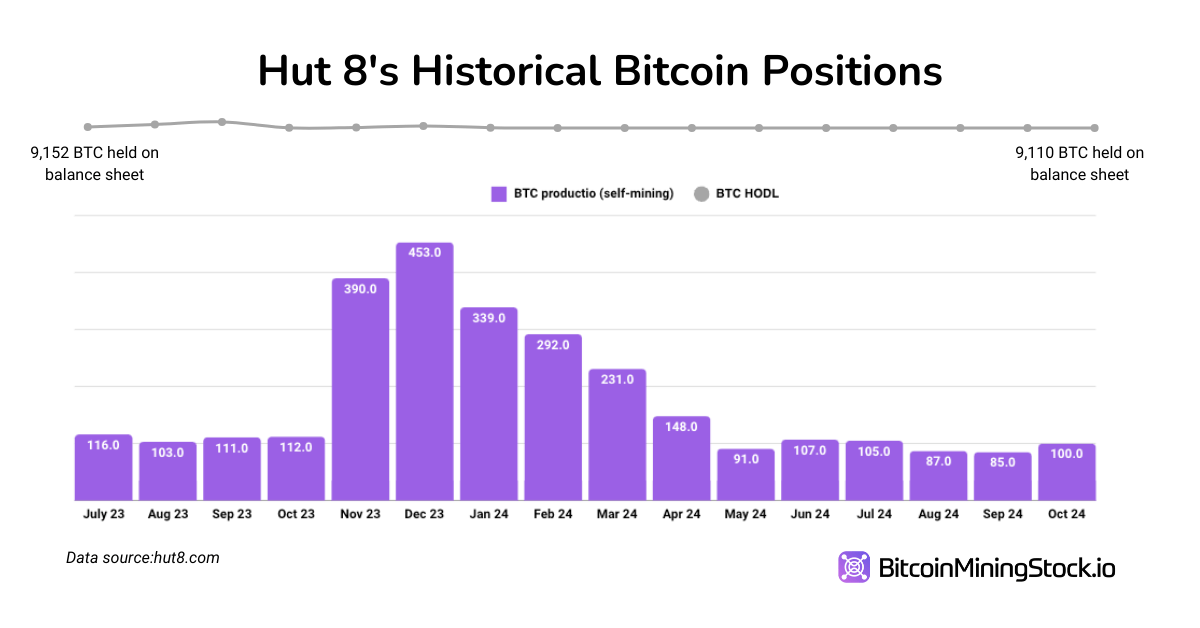

The general public report of Hut 8’s Bitcoin treasury might be traced again to August 2021. All through 2023 and till October 2024, Hut 8’s BTC holdings remained round 9,100 BTC, indicating that the corporate has been periodically promoting newly minted Bitcoin.

Closing Ideas

Earlier this 12 months, investigative analysis firm J Capital Analysis questioned Hut 8’s acquisition of USBTC and the {qualifications} of its management. Regardless of these criticisms, Hut 8 has delivered measurable enhancements: from power effectivity, strategic partnerships to disciplined capital administration and traders can observe tangible adjustments. This veteran Bitcoin mining firm now pivots towards turning into an power infrastructure platform with a spotlight past mining. With Coatue’s funding, its AI and HPC providers are positioned for progress within the coming quarters. Personally, I really feel Hut 8 stays a compelling alternative as a result of its previous and current completely show the right way to adapt and thrive in an ever-evolving business.