The Financial institution for Worldwide Settlements (BIS) warned in regards to the dangers of stablecoin yield merchandise. The addition of yield blurs the road between cost instruments and investments, the group warned.

The Financial institution for Worldwide Settlements (BIS) issued warnings on the enlargement of stablecoin yield merchandise. The group famous the present pattern of stablecoin adoption, however warned about yield-based apps and merchandise.

As Cryptopolitan reported, the BIS has been vital of stablecoins prior to now, alongside a typically adverse stance on crypto.

“These practices could blur the strains between cost devices and funding merchandise. They might compete with financial institution deposits however are sometimes supplied with out equal prudential oversight, deposit insurance coverage and transparency, exposing customers to shopper safety gaps and losses,” warned BIS in a latest evaluation.

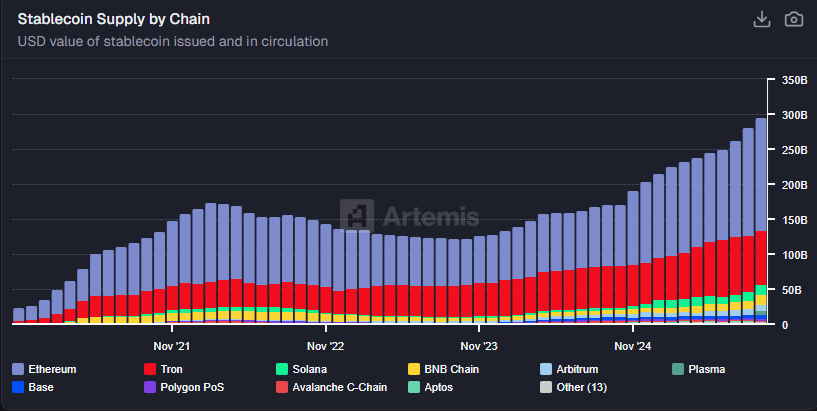

Stablecoins rapidly expanded to a complete provide of 305.9B tokens, cut up between basic cost belongings and specialised tokens linked to yield-based merchandise. The stablecoins are held in 42.1M addresses, up 4% prior to now month.

BIS warns towards conflicts of curiosity for stablecoins and lending companies

The BIS warned that the recognition of stablecoins can set off conflicts of curiosity with conventional banks. Moreover, yield-bearing and lending apps can create conflicts of curiosity. The house remains to be unregulated with regards to yield, regardless of the prevailing framework for stablecoin backing.

The BIS even known as for added rules for decentralized crypto asset service suppliers (CASPs), which give yields. For now, there are not any particular restrictions towards decentralized yield and lending protocols, and no protections for retail customers.

One of many sources of battle is the comparatively increased financial savings charges for some stablecoins, which vastly exceed banking deposit charges for US clients. Nonetheless, the BIS warned that these yield-bearing merchandise had been totally unregulated and had no security mechanisms for depositors.

“Yield-bearing merchandise that mimic financial savings accounts can expose customers to potential losses and hostile contractual outcomes, reminiscent of being handled as unsecured collectors, if the middleman had been to fail,” defined BIS in its latest report.

Some stablecoin protocols faucet the yield from US T-Payments, both straight or by way of tokenized merchandise like BUIDL. In contrast to banks, the protocols are sharing extra of their yields with customers. There are exceptions like USDT, which largely retains the curiosity on its T-Payments.

Aggressive yields depend upon protocols, not stablecoins

Stablecoins are accepted by a number of protocols, and the ultimate yield is determined by these decentralized apps. Even regulated stablecoins like USDC have ended up in high-yield vaults or protocols.

Stablecoins expanded their whole provide, whereas yield alternatives elevated, with extra incentives coming from airdrop farming. Whole stablecoin provide is above 305B tokens. | Supply: Artemis

Many of the liquidity is presently saved on Aave, Morpho, Maple Finance, and Sky Protocol. Nonetheless, there’s a lengthy tail of smaller yield merchandise, with APY above 100% or as excessive as 1,000%. Most merchants nonetheless keep away from these protocols for his or her unrealistic, unsustainable yields.

Extra generally, yields on fashionable protocols vary between 4% and seven%. Even these provides are extra interesting in comparison with financial institution deposits.

Yield from stablecoins usually has extra incentives, reminiscent of airdrop farming. For the previous 12 months, extra customers have chosen to farm new tokens, quite than commerce riskier and extra risky crypto belongings.