Dragonfly Capital closed its fourth fund at $650 million this week, the identical measurement as its 2022 automobile, raised right into a enterprise market Fortune calls a “mass extinction occasion.”

The headline reads like a vote of confidence: institutional capital returning, crypto winter thawing, alt season loading. However peel again one layer and the image warps.

Dragonfly’s companions describe a pivot towards fintech rails and tokenized real-world belongings, with the expectation of fewer “native app tokens.”

This is not a blanket “alts to the moon” sign. It is a guess that worth accrues to companies that do not want tokens in any respect, or to tokens that commerce like asset wrappers quite than reflexive beta performs.

The contrarian learn: VC cash flooding again can reproduce the precise playbook that broke in 2025.

Extra personal capital, deployed into the identical low-float launch buildings that educated markets to front-run unlock calendars, creates extra scheduled promote partitions as an alternative of spot-buying firepower.

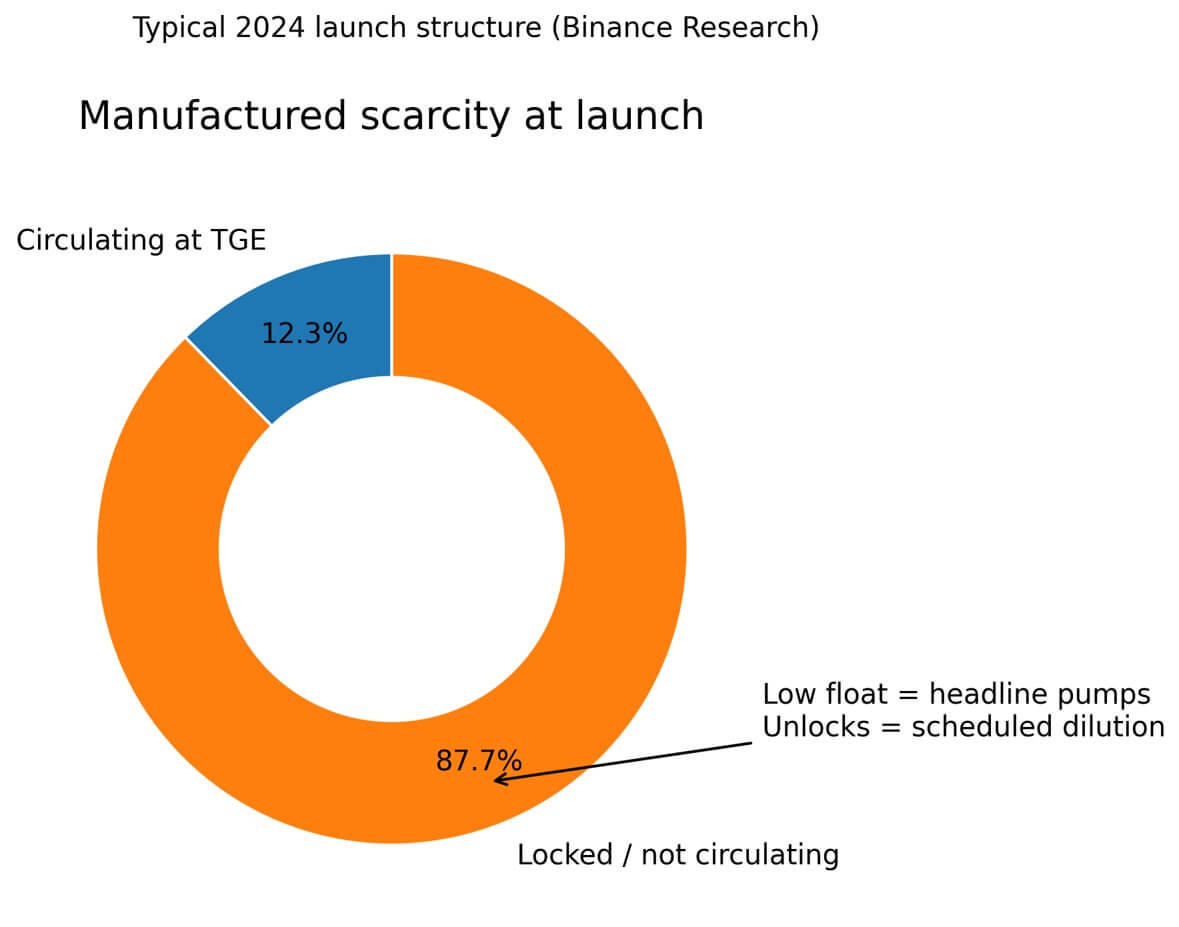

Manufactured shortage, scheduled dilution

The dominant token launch design of the final cycle labored like engineered hype.

Groups launched with tiny circulating provide, usually single-digit percentages of whole issuance, pushing costs skyward at Token Era Occasions whereas locking most allocation behind multi-year vesting schedules.

Binance Analysis tracked 2024 launches and located a median market-cap-to-fully diluted valuation ratio of 12.3%, indicating that patrons bought into buildings through which 87.7% of the availability was locked.

The mathematics was difficult: to maintain costs steady throughout that provide movement, the report estimated the cohort would wish roughly $80 billion of incremental demand-side liquidity.

With out it, each unlock turned a identified dilution occasion.

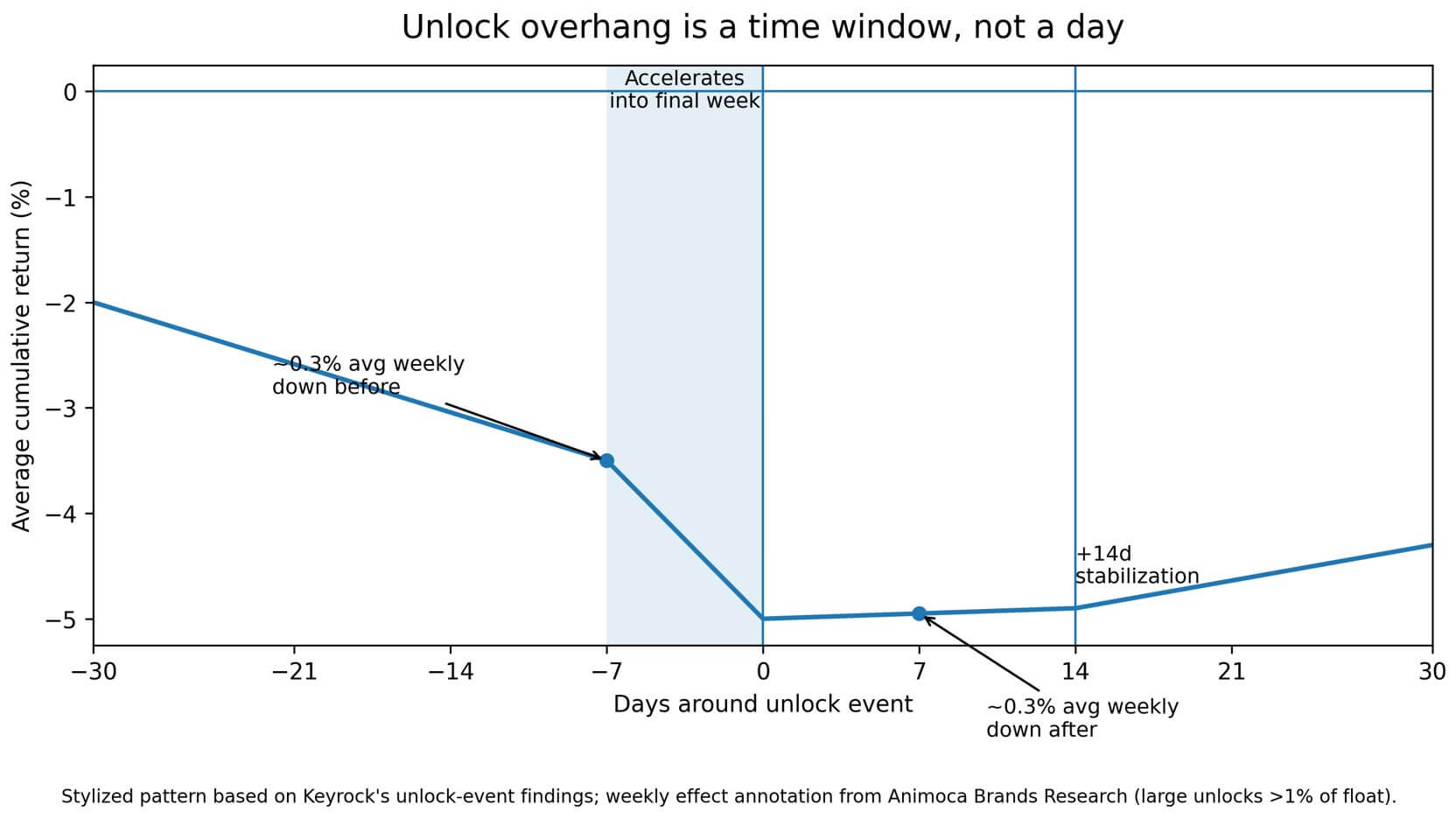

Keyrock analyzed greater than 16,000 token unlock occasions and documented a recurring sample. Drawdowns construct throughout the 30 days earlier than the unlock, speed up into the ultimate week, then stabilize roughly 14 days after.

Animoca Manufacturers Analysis quantified the impact: for unlocks exceeding 1% of the circulating provide, costs decline by a mean of 0.3% within the week earlier than and by one other 0.3% within the week after.

The unlock calendar turns into a everlasting quick thesis baked into the token’s ahead curve.

Memento Analysis’s 2025 launch tracker makes the decision empirical: of 118 tokens that went stay final 12 months, 84.7% now commerce under their TGE valuation, with a median drawdown of 71.1% on a completely diluted foundation and 66.8% on a market cap foundation.

Excessive FDV launches underperformed the equal-weight basket. The larger the hype, the steeper the autumn.

Why “crypto VC funding is again” doesn’t suggest spot shopping for

Dragonfly’s $650 million would not translate into $650 million in market purchases that might raise token costs immediately.

Enterprise funding flows into personal allocations: fairness stakes, Easy Agreements for Future Tokens at discounted charges, and early-stage rounds that give insiders provide earlier than public listings.

The worth assist arrives later, usually structured because the unlock mechanism itself.

Binance Analysis explicitly connects the rise of low-float, high-FDV buildings to inflows of personal capital and aggressive pre-launch valuations.

The identical enter of extra VC cash can reproduce the identical output: extra dilution overhang, extra front-runnable unlock calendars. Dragonfly’s personal thesis reinforces this.

Fortune quotes companion Tom Schmidt describing crypto’s “monetary period,” the place native protocol tokens give method to tokenized shares and fintech rails. That is bullish for sure companies, but it surely implies a world the place upside accrues to fairness or regulated merchandise, to not freely floating alts.

Take this week’s instance. On Feb. 20, LayerZero unlocks roughly $46 million in ZRO tokens, representing 5.98% of the circulating provide and concentrated in insider allocations.

Tokenomist flags it as a near-term overhang in skinny liquidity. That is what “bullish VC” seems like in observe: a public unlock calendar that gives subtle members with a identified exit window and retail holders with a predictable drawdown.

The size drawback

Tokenomist’s 2025 evaluate tallies $97.43 billion of tokens launched throughout the 12 months, cut up into $18.77 billion from insider unlocks and $78.66 billion from non-insider allocations.

For the week of Feb. 16-22 alone, scheduled releases exceed $700 million. This is not background noise, however a structural sell-side movement that dwarfs natural demand in all however probably the most liquid belongings.

Keyrock’s information confirms recipient sort issues, with group and investor unlocks proving extra damaging than ecosystem allocations, seemingly as a result of insiders face fewer coordination prices and clearer revenue incentives.

Binance Analysis warns that with out matching buy-side demand, the trail ahead requires tens of billions in new capital simply to tread water.

Dragonfly’s $650 million, even when absolutely deployed into token offers, represents a fraction of the liquidity wanted to soak up the unlock schedule of tasks already stay.

What good tokenomics really seems like

The response to failed low-float launches is not to get rid of tokens, however to revamp the inducement construction in order that unlocks do not perform as ticking time bombs.

Backpack launched with 25% preliminary float, solely community-facing, and structured the remaining provide round growth-triggered unlocks tied to person progress and protocol milestones.

As an alternative of time-based cliffs, provide launch connects to key efficiency indicators. The market can value optimism or pessimism in actual time, quite than pricing a deterministic provide schedule.

Jupiter allotted 50% of protocol income to token buybacks, making a verifiable sink tied to precise money flows. The group has mentioned concentrating on internet zero emissions in 2026 by restructuring distributions.

Income-linked buybacks convert protocol success into deflationary stress quite than purely dilutive issuance.

USDai’s $CHIP sale allotted 7% of provide to the general public sale, unlocked 100% at TGE, and printed specific mechanics and dates.

The method trades early value stability for radical transparency. There is no hidden insider schedule, no shock vesting tranches. The token launched unstable, however with out the structured sell-wall that depresses costs months later.

Dragonfly’s pivot towards fintech rails provides one other blueprint: some merchandise do not want tokens. If the enterprise mannequin is regulated as a monetary service, forcing a token onto it creates a dilution instrument quite than a helpful asset.

The guidelines

Earlier than shopping for a token, buyers ought to verify 4 metrics: market cap to completely diluted valuation, proportion of provide held by insiders, the scale of the subsequent three scheduled unlocks as a proportion of circulating provide, and the dates these unlocks land.

If the MC/FDV is under 20%, if insiders management greater than half of whole issuance, and if the subsequent unlock exceeds 5% of float, they’re shopping for right into a construction designed to extract worth.

If an investor would not purchase a inventory with a identified 20% share issuance scheduled for subsequent month, then that token is a move, too.

The mechanics are an identical. The return of enterprise funding would not change this, and might even amplify it.

Dragonfly’s $650 million alerts that institutional LPs nonetheless again choose crypto managers, even because the broader enterprise ecosystem contracts.

Nonetheless, whether or not that capital flows into token-heavy offers or into fintech rails, whether or not it reproduces low-float buildings or funds companies that do not want tokens in any respect, determines whether or not “VC is again” interprets to upside for liquid belongings.

The market discovered to cost dilution. The query is whether or not the subsequent wave of tasks discovered the identical lesson.