Cango Inc. pivoted from vehicle buying and selling to Bitcoin mining and is now focusing on 50 EH/s in early 2025. With a rising BTC treasury, Tencent as an institutional investor, and Bitmain hyperlinks, is that this the mining sector’s subsequent darkish horse?

A Cango Deep Dive

The next visitor publish comes from Bitcoinminingstock.io, the one-stop hub for all issues bitcoin mining shares, instructional instruments, and trade insights. Initially printed on Mar. 25, 2025, it was penned by Bitcoinminingstock.io creator Cindy Feng.

It’s been just a few weeks since our final deep dive into lesser-known names within the Bitcoin mining house. I’ve been a bit quiet—partly as a result of the sector’s been in a hunch, but in addition as a result of I’ve been recovering from a lower-back harm (a reminder to hearken to your physique and never push it too exhausting with bodily actions).

For the second instalment of this collection, I need to speak about Cango Inc. (NYSE: CANG). Why? Whereas the entire mining sector has been taking a beating these days, Cango has had just a few sturdy days, boosted by its share buyback announcement and a non-binding buyout provide.

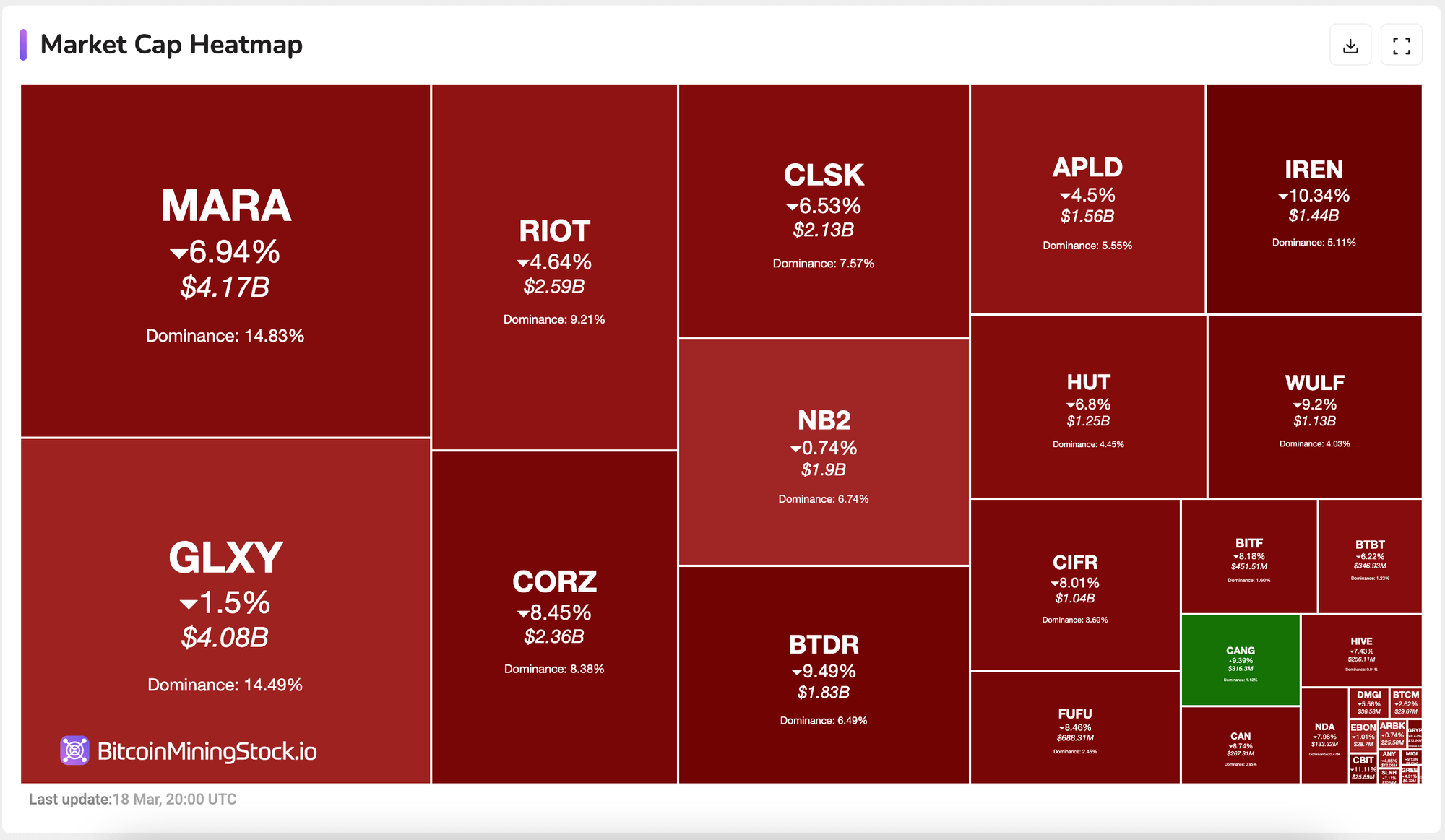

Bitcoin Mining Shares Heatmap (reside updates)

However right here’s what actually caught my eye: just some months in the past, this was nonetheless an vehicle buying and selling platform with restricted progress potential. Now, it focusing on 50 EH/s early this yr, with 32 EH/s already on-line.

So how is that this daring pivot taking part in out? And will Cango quietly develop into a serious participant within the house? Let’s dive in.

Firm Overview

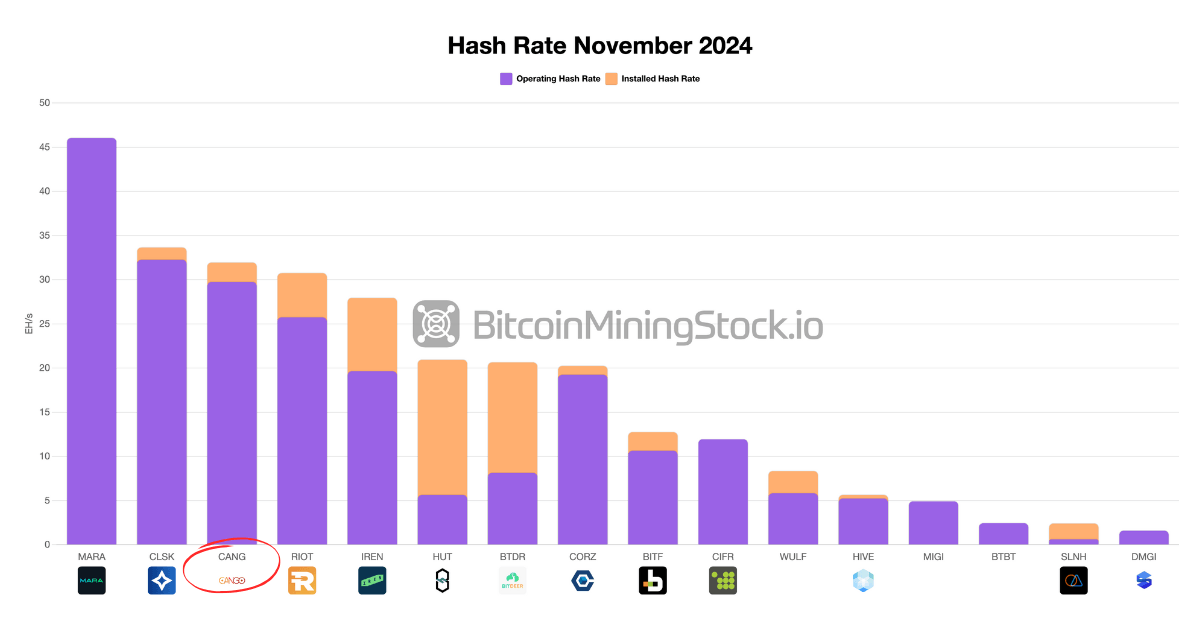

Cango Inc. (NYSE: CANG) started as an Shanghai-based auto financier and later positioned itself as a key participant in China’s vehicle buying and selling companies. By late 2023, the corporate has shifted its focus from the home market to facilitating used automotive gross sales from China to growing markets. Then in November 2024, Cango introduced its entry into Bitcoin mining, launching operations with 32 EH/s of on-line hash charge. The size and immediacy of this transfer shocked many buyers—putting Cango simply behind MARA and CleanSpark, and making it the third-largest public Bitcoin miner by deployed capability on the time.

Overview of Public Miners’ Hash Fee

The mining acquisition deal was for 50 EH/s in complete, with the remaining 18 EH/s anticipated to return on-line in Q1 2025, topic to the efficiency standards outlined within the settlement. Notably, the infrastructure was not constructed from scratch: Cango acquired operational ASIC fleets instantly from Bitmain, and a Bitmain affiliate continues to handle the machines’ operations and upkeep inside third-party internet hosting amenities.

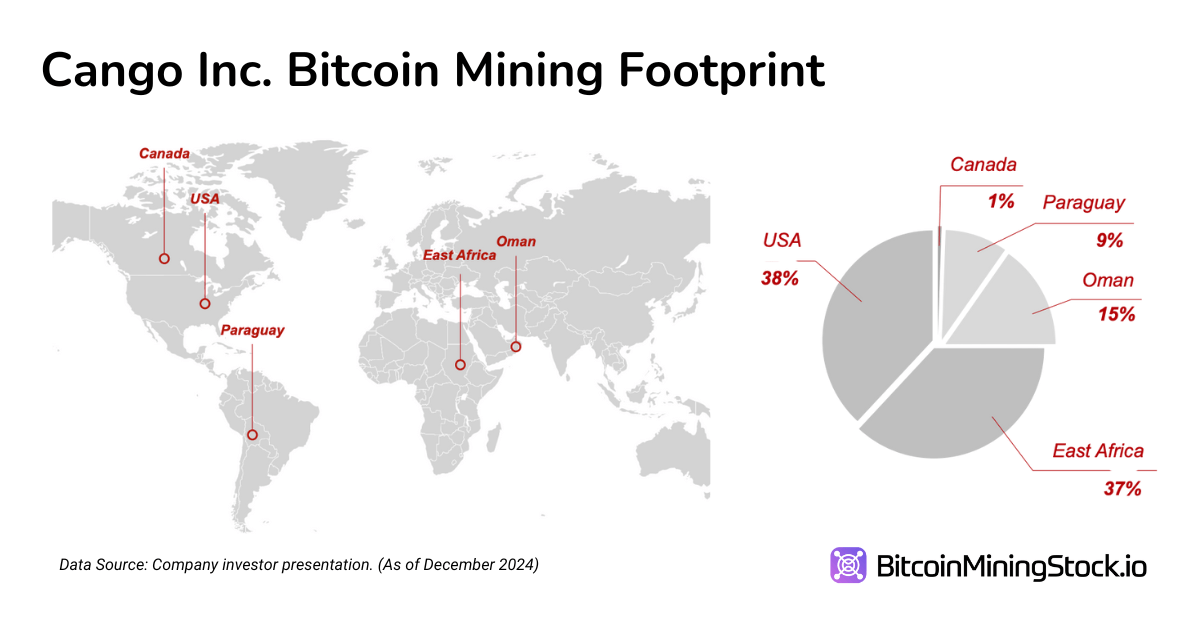

In line with firm disclosures, Cango has its fleet primarily hosted within the U.S.,East Africa, Oman and Paraguay – which retains it clear from China’s ongoing crypto restrictions.

Monetary Highlights

Income & Profitability Transformation

The influence of Cango’s pivot to Bitcoin mining is clearly mirrored in its newest monetary outcomes. In This fall 2024, the corporate reported income of RMB 668 million ($91.5 million), a 414% YoY enhance. This progress was nearly totally pushed by Bitcoin mining, which accounted for 98% of complete income. In distinction, the auto buying and selling phase, as soon as Cango’s core enterprise, simply contributed RMB 15 million ($2.1 million) – a sign that this legacy phase is successfully being phased out.

Regardless of the income surge, profitability stays a key situation. Cango posted a gross margin of 17.6% in This fall—considerably under friends with comparable operational scale. For comparability, CleanSpark, which operates in a comparable hash charge vary, reported a 57% gross margin throughout the identical interval. This implies that Cango’s value construction is way from optimized. Reliance on third-party internet hostingand publicity to greater power prices are two main attributors.

The corporate’s common Bitcoin manufacturing value stood at $67,769 per BTC(money value consists of power and internet hosting charges). This determine locations Cango towards the greater finish of the fee curve amongst massive public miners we observe – lots of whom report all-in prices within the $50K vary. Till Cango secures lower-cost infrastructure or negotiates extra favorable internet hosting phrases, its margin profile is prone to stay underneath strain, even when income progress continues.

Steadiness Sheet & Liquidity

Cango entered 2025 in a robust liquidity place, reporting RMB 2.5 billion ($345 million) in money and short-term investments as of December 31, 2024 – up from RMB 1.7 billion ($232.9 million) the earlier yr. This substantial reserve supplies a significant buffer for continued enlargement and cushions towards potential volatility in Bitcoin markets. Nonetheless, the corporate’s complete liabilities additionally rose sharply, rising 126% YoY to RMB 1.88 billion ($258 million). This rise was primarily pushed by accrued bills and different present liabilities tied to its mining acquisition and associated operations.

Whereas Cango at present has sufficient liquidity to fund near-term progress, the strain now shifts to enhancing operational margins. With out stronger money stream era, the corporate might ultimately want to hunt exterior capital, risking fairness dilution or elevated leverage.

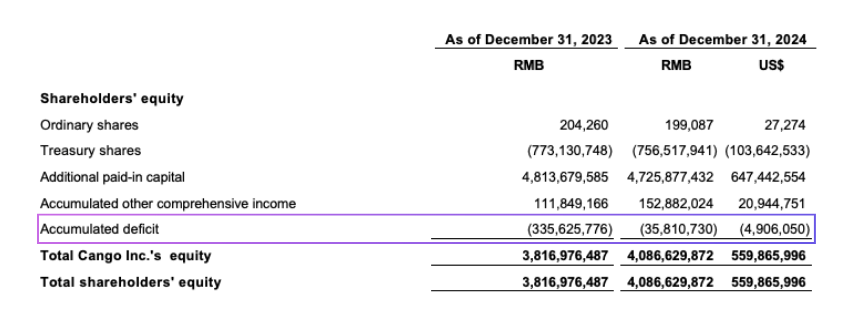

A more in-depth have a look at the fairness construction highlights these trade-offs. Shareholders’ fairness elevated 7.1% YoY to RMB 4.09 billion ($559.9 million), largely as a result of firm’s RMB 299.8 million ($41.1 million) web revenue in 2024. This return to profitability helped cut back the accrued deficit from RMB (335.6) million to RMB (35.8) million, strengthening the steadiness sheet and partially restoring retained earnings.

Nonetheless, the $144 million stock-based part of the $400 million mining machine acquisition considerably impacted fairness construction. It expanded complete fairness but in addition diluted present shareholders as the sellers, now fairness holders, collectively personal roughly 40% of the corporate post-transaction. This possession shift is mirrored within the decline of further paid-in capital from RMB 4.81 billion to RMB 4.73 billion, pointing to a redistribution of fairness slightly than recent capital influx.

Lastly, whereas the corporate repurchased 996,640 ADSs for $1.7 million, the buyback’s influence on complete fairness was negligible. It does, nonetheless, recommend that administration sees the inventory is undervalued, although present capital allocation stays firmly targeted on scaling the mining operation.

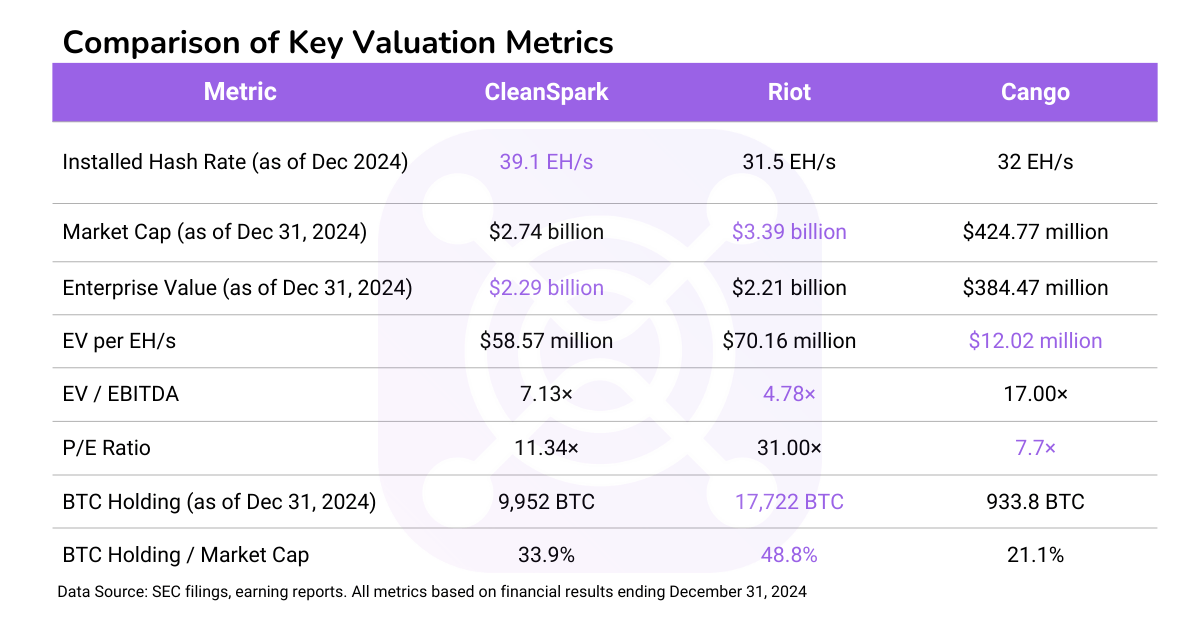

Valuation Modelling

A important step in understanding Cango’s price is to benchmark it towards comparable scale Bitcoin miners (e.g.,CleanSpark, Riot). As of Dec 31, 2024, Cango’s market cap stands at $424.77 million).

- Enterprise Worth (EV): $229.2 million (Market Cap + Debt – Money & Money Equal- BTC Holdings).

- EV/EBITDA Ratio: 17x ($384.47M/$22.8M)

- P/E: 7.7x

- P/S: 2.87x (very reasonable market optimism about income)

- BTC Holding / Market Cap: 21.1%

Mining Operations & Effectivity

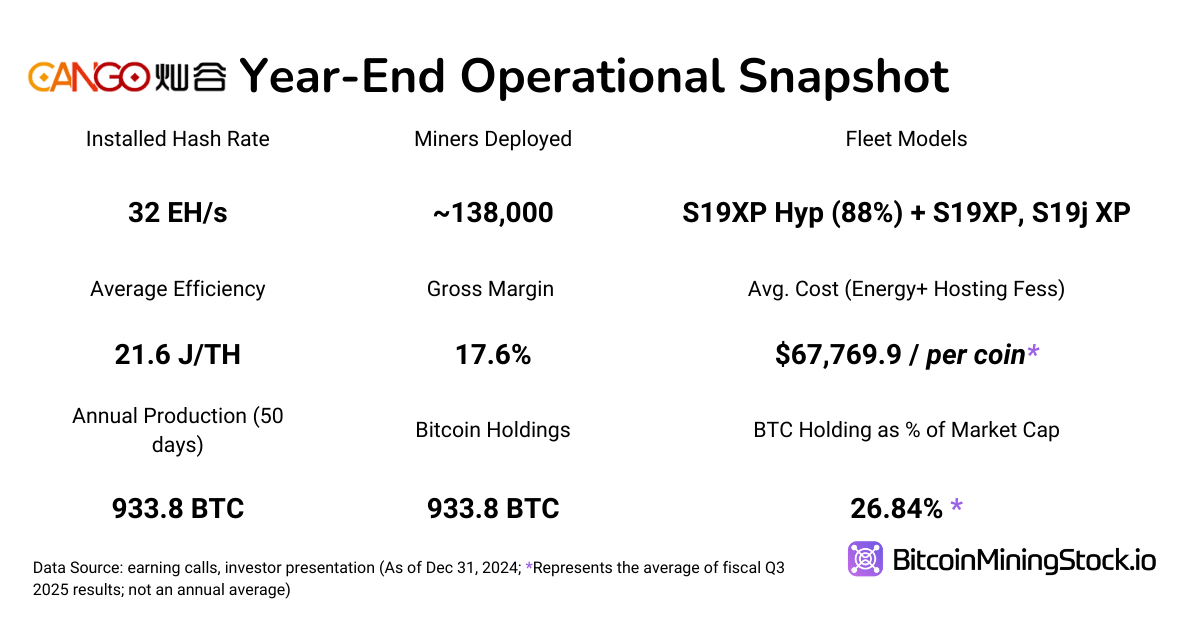

Cango deployed 32 EH/s by December 2024 and is predicted to develop to 50 EH/s in Q1 2025. Projection of Bitcoin manufacturing in 2025:

- Manufacturing charge in This fall 2024: 933.8 BTC in simply 50 days (November-December 2024).

- January-February 2025 replace: 1,010.9 BTC mined, confirming an approximate 500 BTC/month tempo at 32 EH/s.

- Scaling projection: If 32 EH/s produces ~6,000 BTC yearly, then 50 EH/s ought to yield ~8,500 BTC, assuming a linear scaling mannequin.

This projection is a best-case situation, excluding all variables- particularly the community problem. In actuality, rising world hash charge and elevated mining competitors might push community problem greater, which would cut back Cango’s BTC output and have an effect on income forecasts. The corporate’s publicity to such fluctuations is materials, given that just about all of its income is now tied to mining.

Fleet effectivity is one other space of concern. Cango reported an common of 21.6 J/TH, consisting of:

- 90% S19XP Hyd. fashions (water-cooled, environment friendly).

- 10% older fashions (greater energy consumption, much less aggressive).

In distinction, high miners have already begun transitioning to S21 collection {hardware}, which gives considerably higher efficiency and power effectivity.

My Annual Mining Report exhibits that majority of enormous public miners positioned orders for the S21 collection throughout the first 9 months of 2024.

If Cango needs to stay aggressive, it might have to change older machinesand think about migrating from third-party internet hosting to self-operated infrastructure, which may enhance margins over time by lowering internet hosting charges and power prices. With out such enhancements, its greater manufacturing value—already round $67,769 per BTC—may erode profitability in a tightening market.

Bitcoin Treasuries

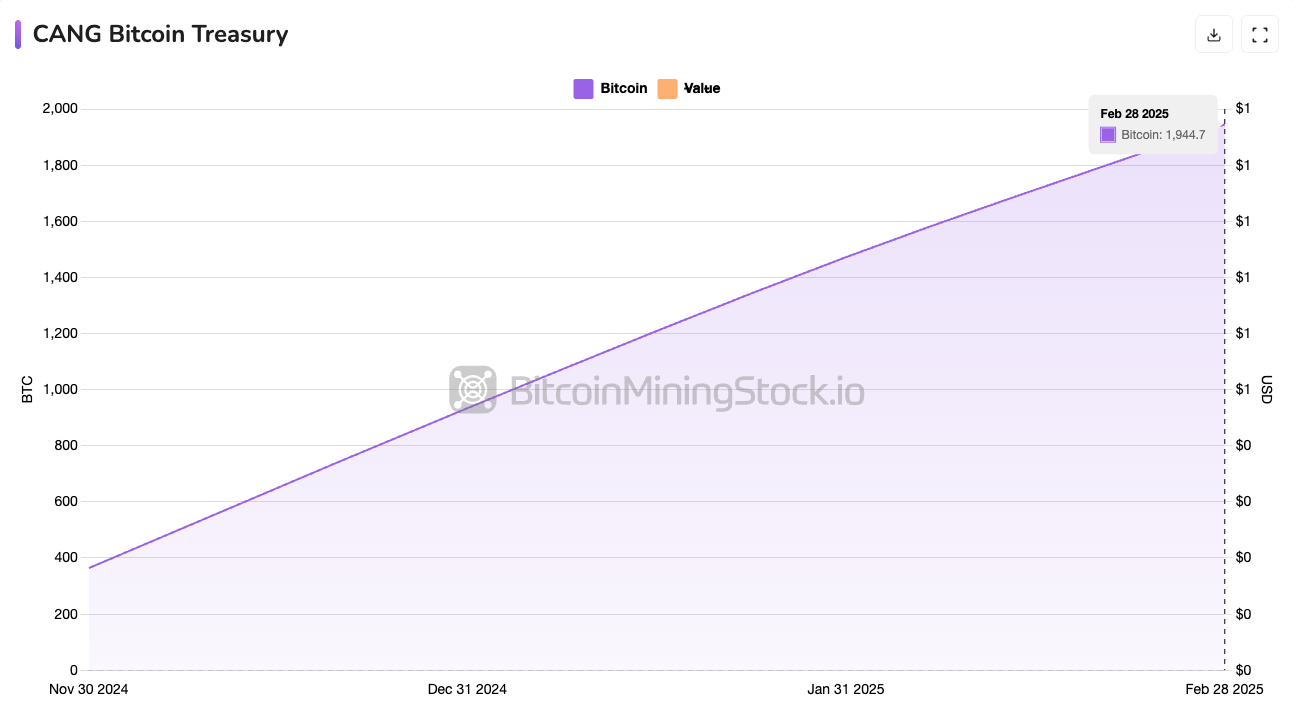

Cango has clearly adopted a “Mine & Maintain” technique, opting to retain its Bitcoin slightly than liquidate for near-term money. As of December 2024, the corporate held 933.8 BTC (~$85 million at year-end costs). By February 2025, that determine had greater than doubled to 1,944.7 BTC, confirming energetic accumulation.

Historic efficiency knowledge for miners is now obtainable in our premium options.

This treasury method gained additional visibility when Cango was added to the Bitwise Bitcoin Commonplace Companies ETF on March 18, 2025—an ETF that tracks public firms holding 1,000 BTC or extra. Inclusion indicators institutional recognition and will enhance visibility amongst crypto-aligned buyers.

Following the earlier assumption, Cango may mine ~ 8,500 BTC in 2025. Coupled with present holdings, its treasury could possibly be ~9,500 BTC by year-end. By then, its Bitcoin holdings may attain practically $1 billion if BTC hits $100K, which doubtlessly locations Cango among the many largest public BTC holders on the planet, rivalling established mining companies and doubtlessly reshaping its valuation narrative.

Whereas this technique aligns with a long-term bullish view on Bitcoin, it introduces liquidity and steadiness sheet dangers. If Bitcoin costs drop considerably, Cango could also be compelled to promote BTC at unfavorable costs or depend on exterior financing to fund operations – particularly for the reason that firm’s mining enterprise remains to be margin-sensitive and capital-intensive.

Non-Binding Buyout Provide: A Hidden Bitmain Play?

On March 14, 2025, Cango acquired a non-binding buyout provide from Enduring Wealth Capital Ltd. (EWCL). Little info is thought about this funding administration firm included within the British Virgin Islands, however key people from EWCL have hyperlinks to Bitmain, the world’s largest ASIC producer.

This raises some hypothesis:

- Is that this an try and separate Cango’s Bitcoin mining enterprise from its Chinese language company origins? Given China’s 2021 mining ban, a construction separation may cut back regulatory dangers and permit Cango to function extra freely.

- Is Cango successfully turning into a Bitmain-backed mining proxy? The corporate purchased the entire fleet from Bitmain’s present operations, with Bitmain associates persevering with to function and keep these machines post-acquisition. Now, Bitmain-linked personnel are behind a buyout try.

If the deal goes via, Cango may have direct entry to Bitmain’s ASIC provide, lowering {hardware} prices and boosting Cango’s aggressive edge, however can also see adjustments in possession construction that have an effect on present shareholders. Traders ought to carefully watch whether or not the deal materializes and what phrases it consists of, because it may essentially alter Cango’s company construction.

Remaining Ideas

Cango’s aggressive pivot into Bitcoin mining has essentially reshaped its company identification. It’s now not an vehicle platform firm with reasonable progress prospects – it now ranks among the many largest Bitcoin miners by hash charge. It has a stack of BTC sitting on the steadiness sheet, which aligns with the rising “Bitcoin Treasury” pattern.

That mentioned, the story remains to be underneath improvement. Core questions stay round operational effectivity , the soundness of Bitcoin costs, and the way successfully Cango can deploy its liquidity to optimize value buildings. For instance, transitioning from third-party internet hosting to self-mining infrastructure, as firms like MARA have carried out, may considerably enhance long-term margins. The current non-binding buyout provide from the entity linked to Bitmain additionally provides intrigue. If deeper integration with Bitmain materializes, it may grant Cango entry to discounted ASIC {hardware} and speed up fleet upgrades,

But challenges persist. Regardless of holding $345.3 million in money and short-term investments, which may cowl roughly 1.13 years of operations at present burn charges, the ageing fleet, primarily composed of second-hand S19 XP Hyd. fashions, faces quicker depreciation. As friends shift to S21 collection machines, Cango might discover itself at an effectivity drawback if it doesn’t hold tempo. Fleet depreciation may additional erode already skinny gross margins, particularly contemplating the This fall report didn’t account for these prices.

Notably, Cango’s management crew brings a sturdy monetary background, and its shareholder base consists of Tencent as a top-11 holder – a truth usually ignored by Western buyers. Nonetheless, its headquarters in China continues to pose regulatory and geopolitical dangers, significantly because the mining ban in China stays in place.

Anybody excited by CANG ought to monitor the next key elements:

- Bitcoin manufacturing value relative to friends

- Depreciation and turnover of older mining fleet

- Liquidity and volatility of BTC holdings underneath a “HODL” technique

- Affect of China-based operations on future strategic flexibility

- End result of the buyout provide and potential reference to Bitmain

Whether or not Cango can set up itself as a key participant within the sector, solely time will inform.