TL;DR

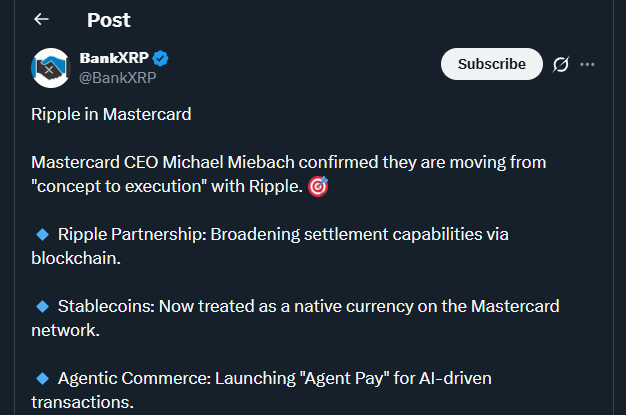

- Ripple strikes into execution part with Mastercard, shifting blockchain settlement from pilots to dwell card cost flows utilizing $RLUSD on the $XRP Ledger, with transactions settling in seconds as a substitute of days.

- Mastercard confirms stablecoins function as a local settlement asset inside its regulated community, preserving client cost experiences unchanged whereas modernizing back-end infrastructure.

-

The rollout begins with the Gemini Credit score Card issued by WebBank, signaling broader institutional adoption of on-chain settlement throughout regulated monetary rails.

Ripple Strikes Into Execution Part with Mastercard marks a transition from experimentation to operational deployment in world funds. The collaboration locations blockchain settlement instantly inside card networks, an space historically dominated by sluggish interbank clearing. For the crypto sector, this improvement reinforces the position of distributed ledgers as core monetary infrastructure fairly than auxiliary expertise.

The transfer follows a pilot launched in late 2025 and enters dwell execution in February 2026. Mastercard executives verify that actual bank card transactions are actually settling by means of blockchain infrastructure fairly than batch-based clearing methods. The method stays invisible to customers, who proceed to faucet or swipe as common, whereas settlement mechanics evolve behind the scenes.

Ripple Strikes Into Execution Part With Mastercard And Dwell Card Settlement

On the heart of the system sits $RLUSD, Ripple’s regulated stablecoin, working on the $XRP Ledger. As soon as Mastercard authorizes a transaction and completes credit score checks, settlement happens on-chain inside seconds. This replaces clearing cycles that usually stretch from one to 3 days between monetary establishments.

The Gemini Credit score Card, issued by WebBank, is the primary product operating on this construction. WebBank’s position as an FDIC-insured establishment offers regulatory oversight, guaranteeing that blockchain settlement aligns with U.S. banking requirements. Mastercard maintains compliance controls according to present card guidelines, integrating crypto rails with out altering client protections.

Mastercard management frames the collaboration as a part of a broader settlement technique. Stablecoins are actually handled as a local settlement foreign money throughout the community, enabling effectivity positive factors whereas preserving regulatory certainty. Alongside this effort, Mastercard continues advancing initiatives similar to Agent Pay, which helps AI-driven transaction execution inside established cost frameworks.

Institutional Adoption And On-Chain Settlement Momentum

Ripple reviews regular development in $RLUSD circulation, pushed by demand from cost and settlement use instances. Provide surpassed $1.3 billion by January 2026, reflecting elevated institutional consolation with regulated stablecoins. Firm executives estimate that by the tip of 2026, between 5 and 10% of capital market settlements function on-chain, supported by comparable enterprise deployments.

This execution part displays a broader trade course. Monetary establishments more and more embed blockchain expertise into present methods as a substitute of constructing parallel crypto-only rails. As Mastercard expands on-chain settlement and agentic commerce instruments, Ripple’s infrastructure positions itself as a connective layer between conventional finance and crypto-native networks, pointing towards deeper integration in world funds.