The CFTC has moved true Bitcoin perpetual futures from an offshore-liquidity debate right into a US-regulated take a look at case, with KalshiEX LLC now accepted to checklist BTCPERP and Coinbase Monetary Markets receiving separate staff-level reduction for entry to sure Deribit merchandise.

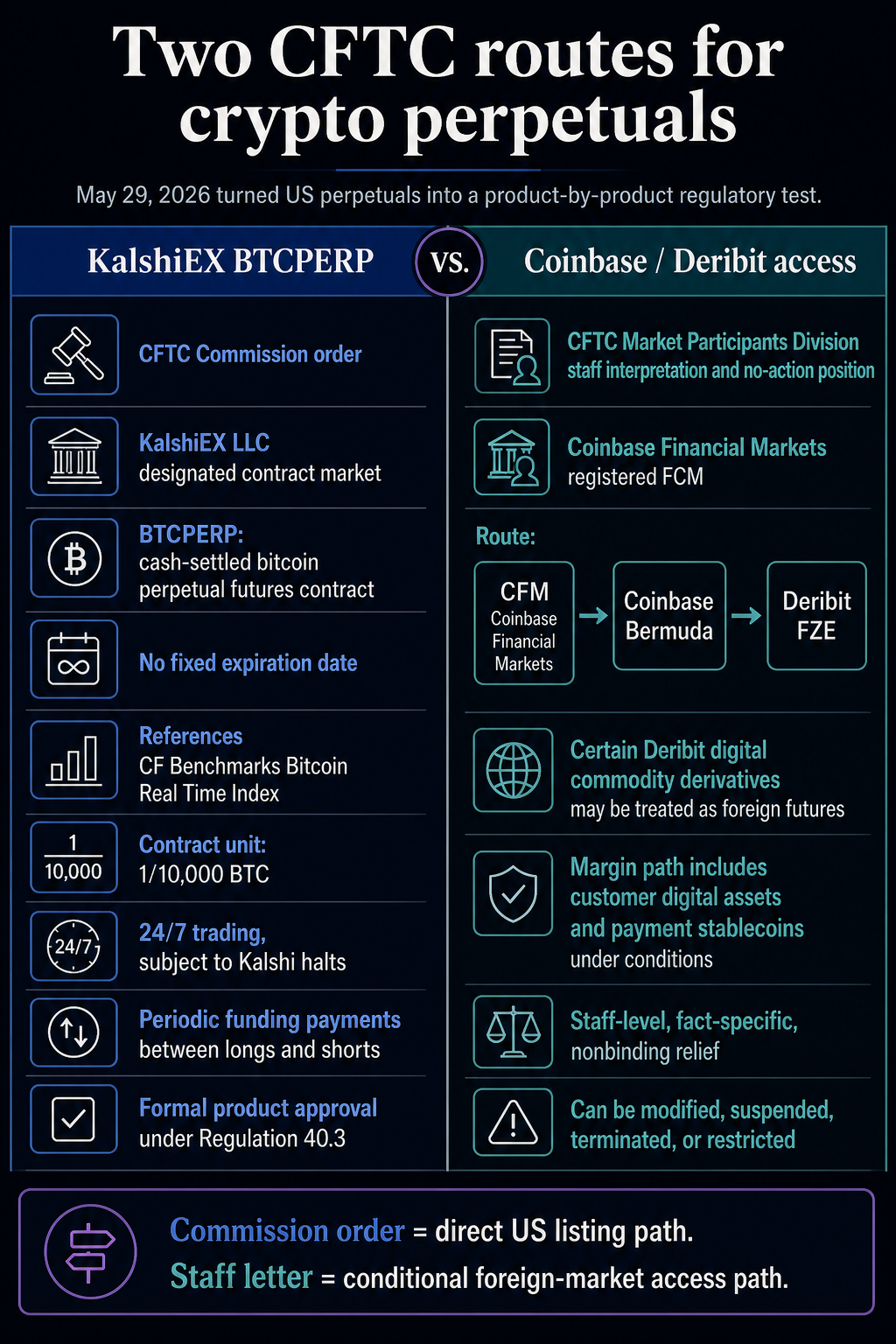

The Fee accepted KalshiEX LLC’s BTCPERP contract as a futures contract, permitting the CFTC-registered designated contract market to checklist a no-expiry bitcoin perpetual tied to the spot worth of BTC.

In a separate transfer the identical day, CFTC workers confirmed that sure Deribit digital commodity derivatives described by Coinbase Monetary Markets could also be handled as international futures when routed via Coinbase’s registered futures fee service provider construction.

Chairman Mike Selig solid the Kalshi order as supply on his pledge to onshore crypto asset perpetuals and as a path for one in every of crypto’s most liquid market segments to exist contained in the US regulatory framework.

Collectively, the actions flip the US perpetuals debate from a theoretical onshoring promise right into a reside market-structure take a look at. One path places a Bitcoin perpetual instantly on a US-regulated change. The opposite provides Coinbase a conditional staff-level route for US shoppers to achieve world crypto derivatives liquidity via its CFM, Coinbase Bermuda, and Deribit associates.

The business response leaned into the market-access level whereas exhibiting how in a different way public firms and exchanges learn the identical CFTC actions.

CFTC steering advances Bitcoin capital markets: 24/7 buying and selling, BTC collateral, perpetual futures, choices, and controlled entry.

Michael Saylor tied the steering to Bitcoin holders and MicroStrategy’s broader Bitcoin-backed credit score technique. Coinbase CEO Brian Armstrong emphasised the customer-access angle and the dimensions of the worldwide market US customers couldn’t beforehand attain via regulated home channels.

Till now, US customers have been locked out of ~80% of worldwide crypto markets.

These reactions are helpful market context. The authorized boundary nonetheless sits within the CFTC order and workers letter.

The excellence is central to the market impression. Perpetual futures are amongst crypto’s most closely traded devices as a result of they let merchants maintain directional publicity with out rolling expiring contracts. The regulatory query is whether or not that construction can match US futures guidelines whereas containing the leverage, liquidation, and collateral dangers that made offshore perps so dominant and so risky.

Two routes opened directly

Kalshi’s approval carries completely different authorized weight as a result of it’s a Fee order. The CFTC issued the order underneath Part 5c(c)(4) of the Commodity Trade Act and Fee Regulation 40.3, discovering that itemizing BTCPERP as a futures contract can be in line with the CEA and the company’s guidelines.

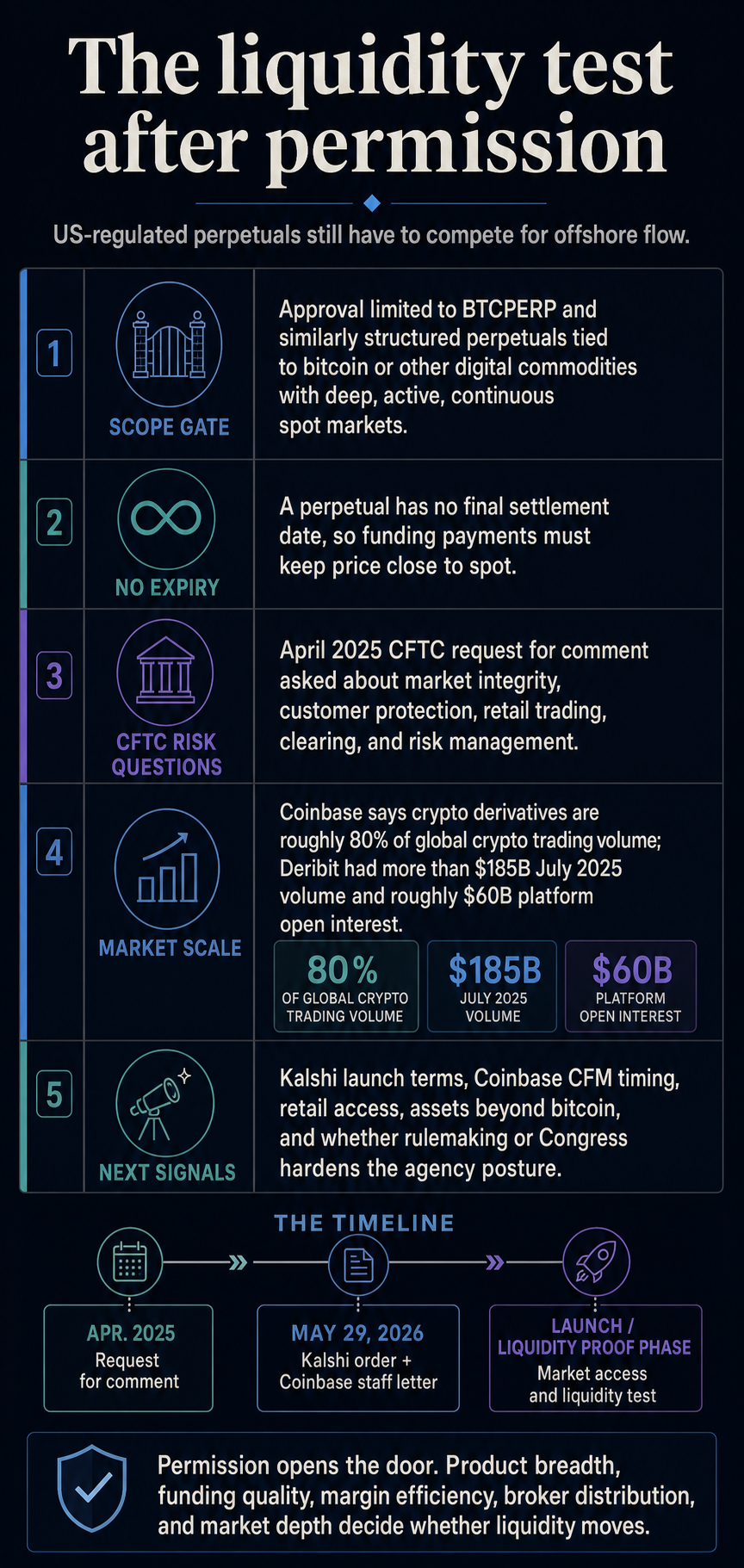

The CFTC launch says Kalshi submitted the contract on Might 29, whereas the order identifies the submission date as Might 28. The approval itself is dated Might 29.

Coinbase’s path is completely different. The CFTC’s Market Members Division issued an interpretation and no-action place in response to Coinbase Monetary Markets. Employees mentioned the Deribit merchandise described within the request could also be categorized as international futures underneath Regulation 30.1.

Employees additionally mentioned it might not suggest enforcement motion underneath specified circumstances tied to buyer digital belongings and cost stablecoins posted as margin via Coinbase associates.

| Path | Regulatory motion | What it covers | Authorized weight | Important restrict |

|---|---|---|---|---|

| KalshiEX BTCPERP | CFTC Fee order | A cash-settled Bitcoin perpetual futures contract listed by a DCM | Formal product approval underneath Regulation 40.3 | Case-by-case reasoning tied to Bitcoin-like market depth and contract design |

| Coinbase / Deribit route | CFTC workers interpretation and no-action place | US buyer entry via CFM to sure Deribit digital commodity derivatives | Employees-level, fact-specific, nonbinding reduction | Conditional construction involving Coinbase associates, international futures guidelines, and margin-collateral safeguards |

That break up shapes sturdiness and scope. The Kalshi route exams whether or not a US change can checklist a perpetual instantly underneath CFTC product approval. The Coinbase route exams whether or not a registered FCM can present US clients with supervised entry to foreign-board-of-trade merchandise whereas assembly circumstances concerning margin, disclosures, and affiliate controls.

Institutional onboarding can start now, choices on Deribit are reside via CFM, and perpetual futures will comply with, based on Coinbase. Broader entry, together with retail, is predicted later, the corporate mentioned.

A Kalshi launch observe described the providing as the primary US perpetuals product and mentioned US traders will quickly have the ability to entry CFTC-regulated crypto perpetual futures on its platform. The corporate additionally mentioned it goals to launch crypto perpetuals on greater than a dozen currencies pending regulatory critiques.

What the CFTC accepted on Kalshi

The Kalshi order describes BTCPERP as a cash-settled by-product referencing the US greenback spot worth of 1 BTC as measured by the CF Benchmarks Bitcoin Actual Time Index. The contract will commerce in items of 1 ten-thousandth of a Bitcoin and may commerce 24 hours a day, seven days per week, topic to Kalshi buying and selling halts.

Its defining function is the absence of a set expiration date. Conventional futures converge to identify at expiry as a result of supply or ultimate money settlement pulls the contract towards the underlying market. A perpetual has no ultimate settlement, so the convergence mechanism should function repeatedly.

The CFTC order says BTCPERP makes use of periodic funding funds between lengthy and quick holders based mostly on the distinction between the contract’s mark worth and the underlying reference worth.

If the contract trades above spot, longs pay shorts. If it trades under spot, shorts pay longs. Fee stress provides merchants an financial incentive to push the perpetual worth again towards the Bitcoin reference worth.

The company’s reasoning relies upon closely on Bitcoin’s market construction. The order says Bitcoin trades repeatedly throughout broadly distributed venues, making the reference worth observable whereas the contract trades. It additionally factors to bitcoin’s deep, lively, steady spot market and to 24/7 spot buying and selling that lets arbitrageurs reply whereas the perpetual trades.

That makes the order consequential and bounded. The CFTC mentioned the evaluation is restricted to BTCPERP and equally structured perpetual contracts that reference Bitcoin or different digital commodities with deep, lively, steady spot market buying and selling. It excludes different asset lessons from the evaluation, and contract categorization stays on a case-by-case foundation.

The novelty caveat retains the authorized significance in focus. CFTC product information present Bitnomial merchandise labeled perpetual futures had been licensed in Might 2026, and Coinbase Derivatives beforehand filed for a nano Bitcoin Perp Fashion Futures product with a long-dated December 2030 expiry.

mycryptopot coated Coinbase’s US perp-style launch in 2025 and later famous that true no-expiry perps differ from long-dated workarounds.

The sensible takeaway: Kalshi has obtained a proper CFTC approval for a real no-expiry Bitcoin perpetual, whereas Coinbase obtained a separate staff-level route for world derivatives entry. That could be a concrete opening for US-regulated perpetuals, with the following approvals nonetheless tied to product design, market depth, and the company’s present posture.

Why Coinbase stays a part of the story

The Coinbase motion has much less sturdiness than a Fee order, nevertheless it may form near-term market entry as a result of it connects US shoppers to Deribit, a venue Coinbase knowledge describe as massive by buying and selling quantity and open curiosity.

Coinbase mentioned crypto derivatives account for roughly 80% of worldwide crypto buying and selling quantity and that US clients have lacked a regulated path to a lot of that liquidity. In a previous investor replace after the Deribit acquisition closed, Coinbase mentioned Deribit had greater than $185 billion in July 2025 buying and selling quantity and roughly $60 billion in platform open curiosity.

The CFTC workers letter is technical as a result of the route is technical. CFM is a registered FCM. It plans to supply clients entry to sure digital commodity derivatives listed on Deribit FZE, described within the letter as an affiliated international board of commerce.

Buyer orders would transfer via Coinbase Bermuda Restricted, an affiliated international dealer, to Deribit.

Employees additionally addressed margin remedy. The no-action place covers specified circumstances the place CFM posts customer-owned digital commodities and cost stablecoins with its international dealer affiliate to margin international futures and choices positions, even the place the international dealer has a proper of re-use over these belongings.

The reduction is tied to circumstances, together with Coinbase possession hyperlinks, disclosures, operational controls, acknowledgments, and use of buyer digital belongings just for margining or securing buyer obligations.

That makes the Coinbase path helpful for distribution and attain whereas leaving a thinner precedential footprint than Kalshi’s order. It exhibits how workers could deal with the foreign-market entry query whereas preserving the Fee’s capacity to revisit the interpretation.

That distinction is sensible for venues, brokers, and clients as a result of it impacts who can depend on the sign and the way rapidly product entry can scale.

The workers letter’s authorized posture is conditional. Its positions characterize the Market Members Division solely, usually are not binding on the Fee or different CFTC workers, depend upon the info offered, and could be modified, suspended, terminated, or restricted.

The liquidity take a look at comes subsequent

The CFTC has been shifting towards this second for greater than a yr. In April 2025, an company request for remark requested about perpetual derivatives, together with their makes use of, advantages, dangers, market integrity points, buyer safety questions, retail buying and selling, clearing, and threat administration.

The transfer additionally matches a broader US push to adapt regulated derivatives plumbing to crypto’s always-on market. mycryptopot beforehand coated CME’s transfer towards 24/7 crypto futures and choices, one other try to scale back the mismatch between legacy market hours and repeatedly traded crypto spot markets.

The company now has two working fashions available in the market: a home change product accepted by the Fee and a staff-cleared international futures entry path via a registered FCM. Each may assist pull some perpetual exercise into supervised US channels. Liquidity nonetheless has to comply with.

These questions stay unresolved. Regulated venues must provide sufficient product breadth, margin effectivity, funding high quality, and dealer distribution to compete with offshore exchanges. If Kalshi’s BTCPERP launches with aggressive funding and entry phrases, and if Coinbase can scale Deribit entry from establishments towards broader shoppers, some movement could transfer into channels the CFTC can monitor extra instantly.

If the merchandise stay restricted, costly, or operationally slower than offshore venues, the approval could carry extra weight as a regulatory precedent than as an instantaneous liquidity shift.

The following alerts are sensible: Kalshi’s launch phrases, Coinbase’s timing for perpetual futures via CFM, the remedy of retail entry, the belongings the CFTC will enable past Bitcoin, and whether or not formal rulemaking or Congress later turns as we speak’s company posture into one thing more durable to reverse.