Is Micron inventory too costly proper now? At round $698 a share, with a 52-week vary stretching from $90.93 to a excessive of $818.67, that query comes up always. The inventory already rallied over 600% from its lows, which sounds extreme on its face. The MU inventory worth goal math, although, tells a reasonably totally different story: a ahead price-to-earnings ratio of roughly 7x to 8x and a PEG ratio close to 0.26 put Micron properly beneath the broader S&P 500 common on a valuation foundation proper now. Whether or not Micron inventory will go up farther from here’s a query Wall Road genuinely splits on, and the reply comes down virtually solely to how lengthy the AI reminiscence scarcity holds.

Micron Inventory Forecast for 2026 and MU Worth Goal Evaluation — Will It Go Up?

The $1,200 Case and Why the Numbers Again It Up

The bull case for Micron inventory not being too costly gained consideration recently. Take the corporate’s trailing P/E of round 39x, multiply it by the consensus fiscal 2026 EPS forecast of $32.45, and also you land at a goal of $1,275. Even the extra conservative EPS estimate of $30.28 on the low finish nonetheless produces a worth of roughly $1,190, a 183% acquire from the place MU was buying and selling on the time. The corporate’s Q1 fiscal 2026 outcomes, reported in late November 2025, supported that type of optimism: income of $13.6 billion, up 57% 12 months over 12 months, DRAM accounting for 79% of the overall, and a gross margin of 45.3%.

The reminiscence scarcity underpinning all of that is additionally actual. Intel CEO Lip-Bu Tan stated the crunch is not going to ease till 2028. And in its Q1 fiscal 2026 earnings name, Micron’s personal administration made the size of the demand drawback very clear:

“Regardless of vital efforts, we’re upset to be unable to satisfy demand from our clients, throughout all market segments. We’ve got accomplished agreements on worth and quantity for our whole calendar 2026 HBM provide, together with Micron’s industry-leading HBM4.”

Promoting out a whole calendar 12 months of HBM provide is a reasonably outstanding knowledge level by itself, and it additionally explains why analysts maintain lifting their MU inventory worth targets. On the time of writing, the three most up-to-date upgrades got here from Citigroup ($840), Melius Analysis ($1,100), and Mizuho ($800), all on Could 19, placing the typical of these three alone at over $913.

Why Ought to You Purchase MU Inventory? What Analysts Say In regards to the MU Inventory Worth Goal

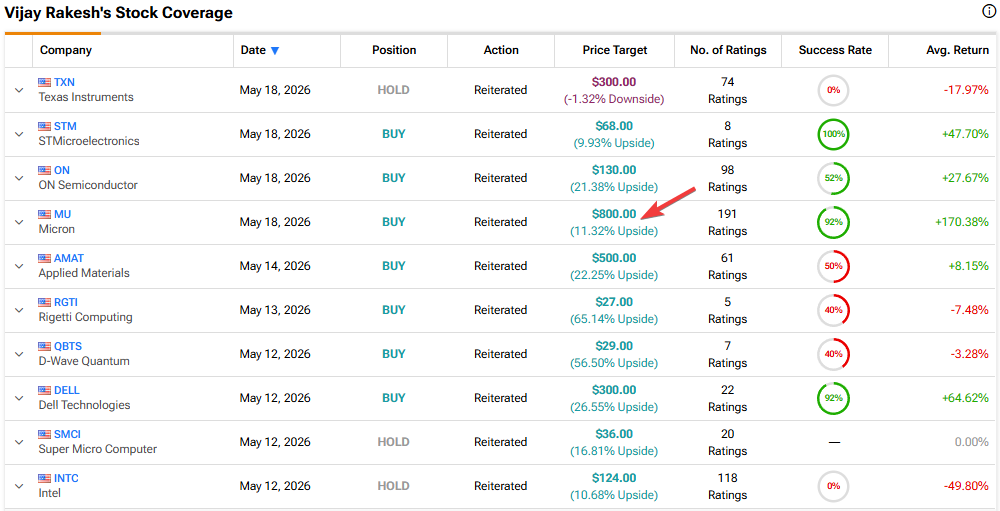

Mizuho’s Vijay Rakesh, one of many extra constantly bullish voices on Micron inventory, raised his MU inventory worth goal to $800 from $740 and saved an Outperform ranking. He argues pricing power in NAND and DRAM markets will final properly past this 12 months.

Rakesh wrote in his Could 19 analysis word:

“We proceed to notice pricing tailwinds in 2026 from AI server demand as we see NAND pricing up 413% y/y and DRAM up 355% y/y. We word potential for additional pricing tailwinds for Micron as a possible Samsung strike looms, whereas Micron additionally is anticipated to report Could-quarter earnings on June 24.”

In an earlier word, Rakesh additionally pointed to “agentic AI driving reminiscence demand increased,” and projected HBM income rising at a 40% compound annual charge to surpass $100 billion by 2028. His fiscal 2027 estimates name for income development of 66% and EPS development of 80%, 12 months over 12 months.

Will Micron Inventory Go Up, or Is a Correction Coming First?

Not everybody shares that optimism. In search of Alpha analyst Victor Dergunov, who purchased MU shares within the $106 to $119 vary in 2025, downgraded the inventory to Promote on Could 18, citing parabolic worth motion and a market cap closing in on $1 trillion.

Dergunov acknowledged in his downgrade word:

“Whereas Micron may go to $1,000 or $1,200 or probably even increased if the reminiscence scarcity persists and the market stays in FOMO mode, it’s extremely unlikely that Micron may maintain its worth elevated round there. Actually, there are lots of shares that seem as an instance bubble-like behaviors, however Micron and Sandisk particularly.”

Is It Too Late to Purchase Micron? A Correction to The $500 to $600 Vary

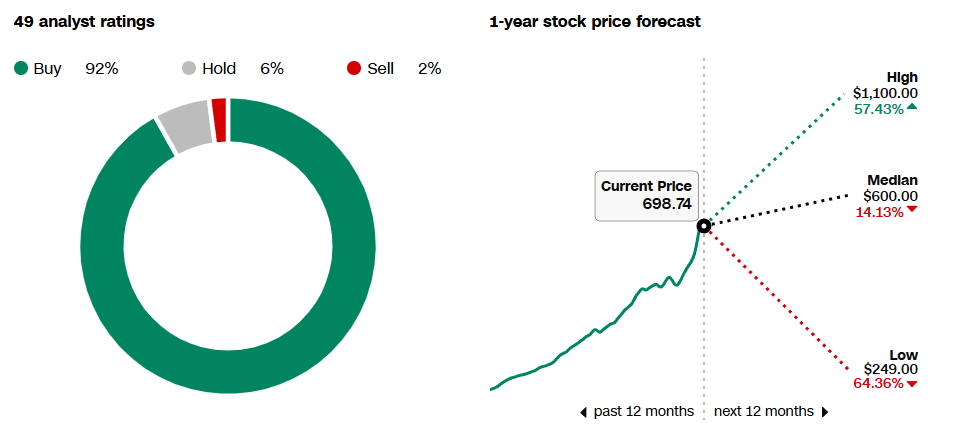

Dergunov’s near-term name sits at a correction to the $500 to $600 vary. The broader bear case rests on a simple historic argument: the reminiscence market has at all times normalized finally, provide catches as much as demand, pricing energy fades, and margins compress. Micron additionally faces actual competitors from Samsung and SK Hynix, each of that are ramping capability aggressively proper now. The typical 12-month analyst worth goal throughout the complete protection universe sits at round $600, which truly implies draw back from the place MU trades at this time.

Macro headwinds add to the stress. The 30-year Treasury yield hit 5.198% on Tuesday, its highest since July 2007, and that type of charge setting tends to weigh on tech shares priced on future earnings. CEO Sanjay Mehrotra additionally bought 40,000 shares at $536 in early Could, and insiders general moved round 106,000 shares value roughly $47 million over the previous three months.

So is it too late to purchase Micron inventory? That basically relies on which a part of the story you discover extra convincing. The bull aspect, that Micron inventory just isn’t too costly right here, rests on a structural reminiscence scarcity with no near-term repair, a valuation that also seems to be low cost on a ahead foundation, and a place as the one main American DRAM producer in a three-player world market. The bear aspect says a inventory buying and selling close to a $1 trillion market cap in a cyclical, commoditized {industry} already has a whole lot of excellent news baked in. Each arguments maintain water, and that rigidity is precisely what makes the MU inventory worth goal debate so laborious to name heading into the second half of 2026.