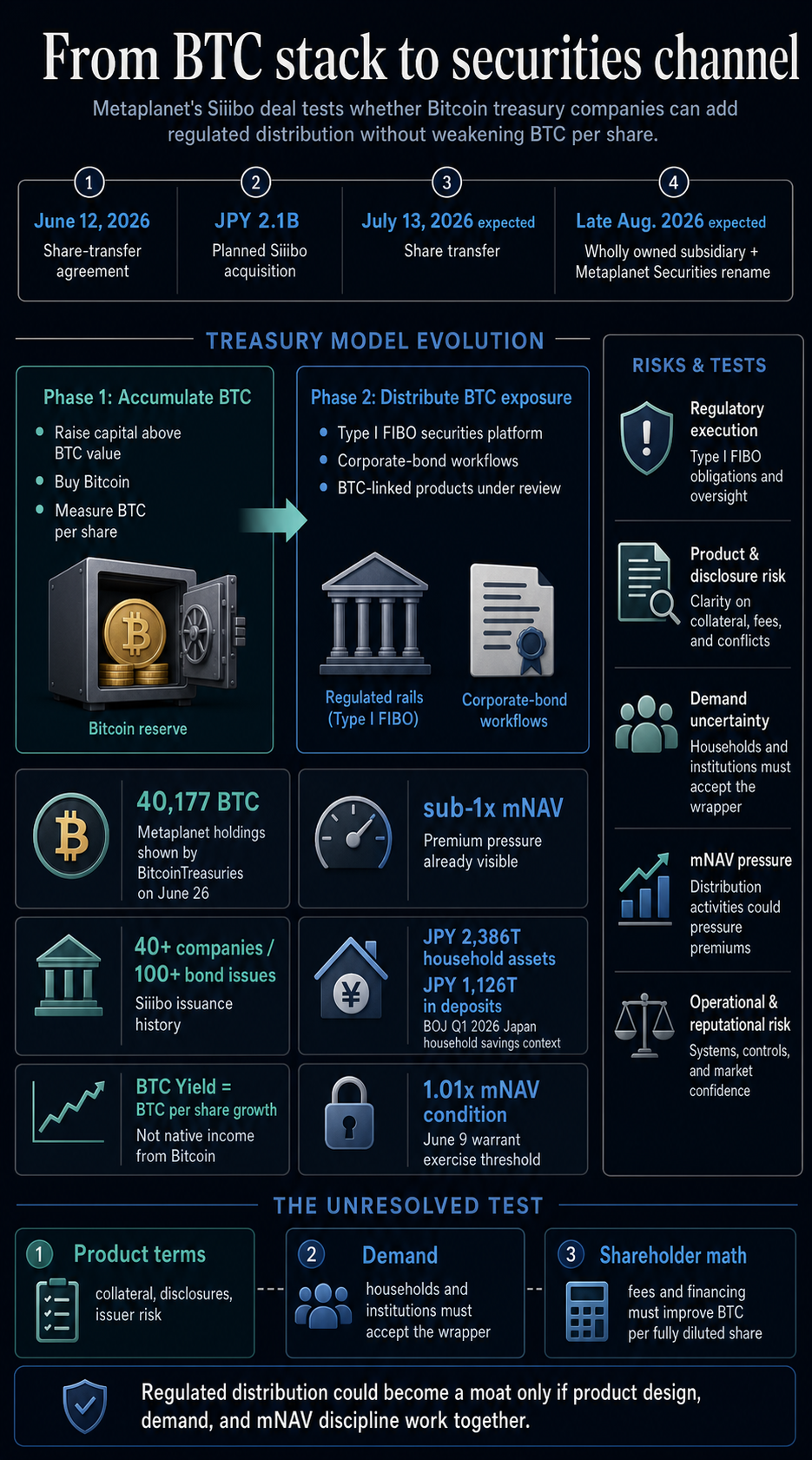

Metaplanet’s Siiibo deal turns the Bitcoin treasury commerce from a balance-sheet accumulation query right into a regulated distribution take a look at.

The Japan-listed firm has agreed to accumulate Siiibo Securities, a regulated corporate-bond platform, giving Japan’s largest public Bitcoin treasury firm a route into securities structuring and distribution whereas mNAV, dilution, and BTC-per-share math are beneath strain.

The broader query has shifted from copying a easy treasury playbook to constructing licensed channels that may bundle Bitcoin publicity whereas preserving the per-share BTC declare that made the commerce engaging within the first place.

Metaplanet’s June 12 disclosure stated it had executed a share-transfer settlement to accumulate Siiibo for JPY 2.1 billion, with the share switch anticipated on July 13 and conversion into an entirely owned subsidiary anticipated in late August, topic to the required procedures.

The corporate stated Siiibo is anticipated to be renamed Metaplanet Securities after closing.

BitcoinTreasuries’ Metaplanet profile, seen June 26, confirmed the corporate holding 40,177 BTC whereas its fundamental and diluted mNAV figures sat beneath 1x.

In that setting, the Siiibo deal turns into a take a look at of whether or not a treasury firm can construct a enterprise round its Bitcoin publicity as a substitute of relying primarily on repeated equity-linked financing.

Regulated rails and per-share Bitcoin

Siiibo provides Metaplanet a securities platform with a regulatory report and an working historical past. Japan’s Monetary Companies Company lists Siiibo Securities as a Monetary Devices Enterprise Operator, and Metaplanet describes it as a registered Sort I Monetary Devices Enterprise Operator working a web based platform centered on company bonds.

Metaplanet’s supplies say Siiibo has supported bond issuance, underwriting, and solicitation for greater than 40 corporations and greater than 100 bond points.

That report has operational worth as a result of the acquisition brings greater than a authorized standing. It brings issuance workflows, compliance processes, issuer relationships, and investor-facing distribution expertise.

The corporate’s supplemental deck is express concerning the route. Metaplanet framed the acquisition round “Bringing Yield to Japan” and stated it intends to discover income-oriented BTC-linked merchandise, personal placement debt merchandise, merchandise incorporating Bitcoin-related property, and digital monetary merchandise equivalent to safety tokens by way of the Siiibo channel.

These stay product ideas beneath evaluation, reasonably than launched merchandise, but they present the strategic form of the transfer.

For a Bitcoin treasury firm, the distinction is materials. A passive treasury mannequin is dependent upon entry to capital and the market’s willingness to worth the corporate above its BTC.

A securities platform creates the opportunity of charges, distribution, product design, and direct entry to buyers who might want Bitcoin-linked publicity in a regulated wrapper.

The yield language additionally wants a exact denominator. On its about web page, Metaplanet says BTC Yield is a key efficiency metric, and defines that metric as progress in Bitcoin per share.

That metric measures balance-sheet accretion reasonably than revenue paid by Bitcoin itself.

If Metaplanet ultimately affords yield-style Bitcoin merchandise, the revenue must come from a disclosed construction round BTC, equivalent to credit score unfold, collateralized lending, choices premium, issuer danger, tokenized-security mechanics, or one other acknowledged mechanism.

Bitcoin itself produces no native coupon.

Metaplanet’s June 9 warrant disclosure exhibits why that distinction is central to the mannequin. The corporate revised the ground train phrases for its twenty seventh Sequence inventory acquisition rights in order that workouts stay doable solely when mNAV is not less than 1.01x.

Metaplanet stated the situation was meant to keep away from workouts that had been unlikely to extend Bitcoin per share and will create dilution.

That’s the identical strain each treasury firm faces when straightforward premiums fade. If shares commerce at a big premium to BTC worth, issuance may be accretive.

If the premium compresses or disappears, the identical financing instruments can dilute the prevailing declare on the Bitcoin stack.

A product enterprise might add a second engine, but it must be judged in opposition to the identical denominator: BTC per totally diluted share after charges, debt, most popular claims, and working prices.

Japan’s financial savings market modifications the route

Metaplanet’s playbook diverges from Technique’s capital-market mannequin by including a licensed Japanese securities platform and bond-product ambitions.

Technique stays the reference level for the size model of public-company Bitcoin accumulation, however Metaplanet’s Siiibo transfer is extra home and distribution-led.

It’s constructed round regulated securities distribution, company bonds, and a financial savings market with an unusually giant money base.

The Financial institution of Japan’s preliminary first-quarter 2026 flow-of-funds information present households held JPY 2,386 trillion in monetary property on the finish of March, together with JPY 1,126 trillion in forex and deposits.

That deposit-heavy base explains why an organization would need regulated rails for yen-denominated or Japan-distributed Bitcoin-linked merchandise.

A big financial savings pool alerts an addressable market, reasonably than confirmed demand.

The ultimate product phrases will determine whether or not the proposition is simple publicity, structured credit score, leveraged yield, tokenized claims, or one thing nearer to an issuer-risk product with Bitcoin branding.

That’s the place the treasury commerce turns into extra difficult. A listed firm can maintain Bitcoin in a approach shareholders can monitor.

A regulated product platform can broaden entry and maybe create payment revenue, whereas additionally introducing product-level danger, disclosure obligations, distribution suitability questions, and potential liabilities which might be separate from the BTC reserve itself.

The broader public-company Bitcoin treasury class has additionally grown giant sufficient for these inquiries to matter throughout multiple issuer.

BitcoinTreasuries tracks roughly 199 public corporations holding about 1.264 million BTC, making capital construction and valuation self-discipline greater than a single-company difficulty.

Latest protection of treasury-company shareholder prices and Technique’s lending pivot has already moved the controversy past headline accumulation into financing phrases, dilution, most popular claims, and whether or not BTC per totally diluted share really improves.

Metaplanet’s acquisition provides a brand new model of the identical debate: if treasury corporations want working companies round Bitcoin, the standard of these companies will matter as a lot as the dimensions of the BTC pile.

Product design shapes the end result

Metaplanet’s Siiibo transfer suggests Bitcoin treasury corporations are testing a shift from accumulation autos into financial-product corporations.

The sting would come from licensing, distribution, belief, issuer relationships, and product design, together with being early to carry BTC on a public stability sheet.

That may be optimistic for Metaplanet if the corporate makes use of Siiibo to construct clear, well-priced merchandise that create income whereas supporting the BTC-per-share technique.

It will probably additionally create new danger if yield language pulls buyers into buildings the place the return is dependent upon leverage, credit score publicity, collateral phrases, or issuer obligations which might be tougher to know than spot Bitcoin publicity.

The following checks are concrete. The July 13 anticipated share-transfer date and late-August subsidiary conversion will present whether or not the platform acquisition closes as deliberate.

Product filings, time period sheets, collateral guidelines, danger disclosures, distribution limits, and buyer demand will present whether or not Metaplanet Securities turns into an actual working engine.

For the broader treasury sector, the lesson is bigger than one Japanese deal.

When mNAV premiums are wealthy, the mannequin can look easy: difficulty shares, purchase Bitcoin, repeat. When premiums compress, corporations want a stronger reply.

Metaplanet is making an attempt to reply by way of licensed distribution and yield-style product design.

The end result will rely upon whether or not these regulated channels enhance the economics shareholders really personal.

In the event that they create sturdy charges, disciplined product demand, and accretive BTC-per-share outcomes, securities distribution may develop into the following moat for Bitcoin treasury corporations.

In the event that they principally add complexity round a risky reserve asset, the market might deal with the transfer as one other type of leverage wearing a regulated wrapper.