Placing $1000 in Micron inventory at precisely the precise second become roughly $468,000. On November 21, 2008, MU shares crashed to an all-time intraday low of $1.59 in the course of the depths of the worldwide monetary disaster, and traders who purchased there and held by means of right now’s worth close to $751 are sitting on returns north of 46,000%. That type of Micron inventory efficiency is uncommon. Proper now, with the AI reminiscence supercycle reshaping the complete semiconductor trade, the query is whether or not the Micron inventory valuation hole and structural HBM demand can energy one other historic run for (NASDAQ: MU).

Micron Inventory Development Potential, Valuation Hole and Efficiency Outlook

The Returns That Constructed MU’s Legend

Even traders who missed the 2008 backside had a second shot. MU fell to $90.93 in spring 2025, throughout a broad market pullback that rattled loads of conviction-heavy holders. From that entry alone, the inventory surged to an all-time excessive of $818.67, additionally a achieve of over 700% in below a yr. So $1000 in Micron inventory at that secondary low is, on the time of writing, value round $8,200. The inventory sits close to $751 proper now, with its complete 2026 HBM provide already spoken for and no significant new capability arriving earlier than 2028.

| Entry Level | Share Worth | Approx. Return |

|---|---|---|

| All-time low — Nov 21, 2008 | $1.59 | >46,000% |

| Dot-com crash backside — Jul 24, 1996 | $8.62 | >9,000% |

| Latest pullback — spring 2025 | $90.93 | >700% |

What Micron’s CEO Has Been Saying

Micron CEO Sanjay Mehrotra has not been delicate concerning the provide image. On the Q1 FY2026 earnings name, he acknowledged:

“The hole between the demand and provide for all of DRAM, together with HBM, is de facto the best that we have now ever seen. We have now accomplished agreements on worth and quantity for our complete calendar 2026 HBM provide.”

He additionally famous that Micron can at the moment meet solely about 50% to 66% of demand from its key prospects, and that tight situations in each DRAM and NAND will stretch into 2027 or past. That could be a fairly exceptional factor for a significant chip firm to say out loud. In fiscal Q2 FY2026, the corporate posted income of $23.86 billion, up 196% yr over yr, alongside document gross margins. On the earnings launch, Mehrotra added:

“Micron set new information throughout income, gross margin, EPS, and free money move in fiscal Q2, pushed by a powerful demand atmosphere, tight trade provide, and our sturdy execution. Within the AI period, reminiscence has grow to be a strategic asset for our prospects.”

The Valuation Hole Wall Road Has Not Absolutely Closed

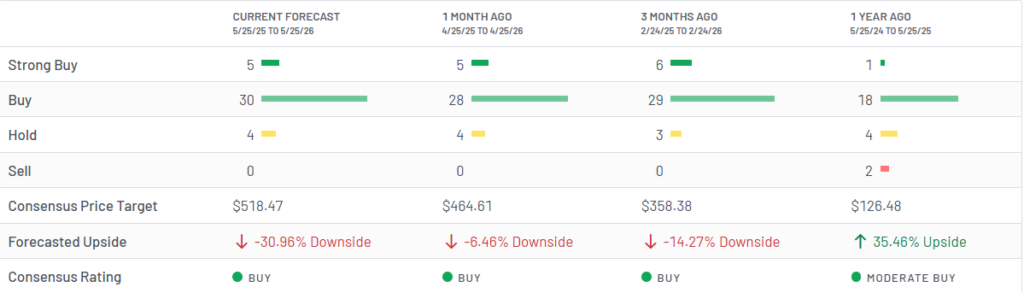

Based mostly on 39 Wall Road analysts who’ve issued scores previously 12 months, MU carries a consensus “Purchase” ranking: 30 purchase, 5 sturdy purchase, 4 maintain, and 0 promote. The consensus 12-month worth goal sits at $518.47, which suggests roughly 31% draw back from $751. The Micron inventory valuation hole between the place the inventory trades and the place the common analyst places it displays an actual break up, with a part of Wall Road nonetheless operating previous memory-cycle fashions and one other half pricing in a structurally totally different AI demand atmosphere. Deutsche Financial institution and DA Davidson each raised their targets to $1000, HSBC to $1100, whereas essentially the most cautious goal on the Road sits at $155.

Any Micron inventory evaluation constructed on ahead earnings tells a special story. The inventory trades at roughly 10x ahead earnings, with EPS forecast to develop round 34% yearly and projected return on fairness close to 49% over the subsequent three years. Cloud reminiscence and AI knowledge middle income now drive the dominant share of the enterprise, and Micron inventory development potential ties on to how lengthy HBM demand stays forward of provide.

Placing $1000 in Micron inventory right now is a special wager than it was in 2008 and even in spring 2025. The inventory has already run exhausting and Micron inventory efficiency over the previous yr has been extraordinary. However the provide math, with the demand-supply hole on the highest stage Mehrotra says he has ever seen, is the type of structural situation that has traditionally rewarded persistence. Whether or not a 3rd re-rating comes or not will in all probability rely on three issues: HBM demand staying structurally forward of provide, the corporate changing that tightness into increasing margins, and earnings persevering with to outpace already-elevated expectations from right here.