Stablecoin funds expanded in 2025, with a rising share of B2B transfers. In response to Artemis, the tokens noticed 70% extra utilization as a fee software since February.

In 2025, stablecoin funds expanded by over 70% since February. The fiat-pegged market advanced, with funds changing into one of many key vectors of growth, with Circle’s USDC main the pattern.

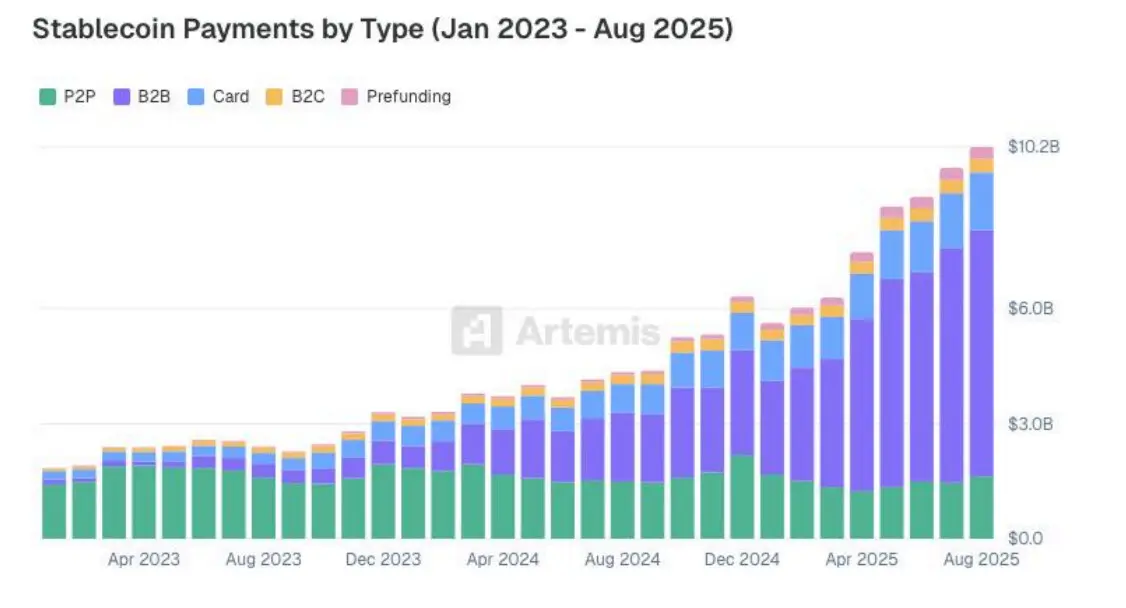

Artemis, one of many main crypto information hubs, collected information from 22 crypto fee firms to estimate the real-life utilization of stablecoins. A further 11 startups had been interviewed for further information, coming from B2B, P2P, B2C, card fee, and prefunding funds.

The information assortment tracked $136B in funds between corporations, settled between January 2023 and August 2025. The time interval already confirmed the evolution of the stablecoin market, as developments continued into Q3, with expanded provide and energetic customers.

B2B funds dominated the market

Artemis found B2B funds had been the most important increase to exercise, because the belongings enable giant, permissionless settlements. Such a funds reached $76B annualized, whereas P2P funds got here second with $19B per 12 months.

B2B funds had been probably the most energetic phase for stablecoin utilization. App and card funds expanded in 2025, displaying mainstream retail adoption. | Supply: Artemis

Crypto playing cards adopted in recognition, with $18B in annual settlements. B2C funds had been at $3.3B, whereas prefunded fee options settled $3.6B.

Regardless of the rising affect of USDC, Tether’s USDT was nonetheless the preferred token utilized by corporations. USDT had a 85% market share by quantity, with Circle coming second. TRON carried the most important stablecoin volumes, adopted by Ethereum, BNB Chain, and Polygon.

The USA, Singapore, and Hong Kong posted the most important switch volumes for funds.

Cost options boosted stablecoin utilization

One of many components for the elevated utilization of stablecoins had been the fee apps constructed by centralized exchanges. Most notably, Bybit Pay and Binance Pay emerged as exercise hubs, tapping their alternate prospects with further switch instruments.

BVNK additionally emerged as a fee gateway, with infrastructure linking banks and blockchains. BVNK focuses on the scalability issues of companies. The method of BVNK is to permit companies to make use of fiat, then full the stablecoin transactions on the backend, utilizing the quick, borderless infrastructure.

Stablecoin playing cards had been the opposite issue to spice up mass adoption. With clearer rules, card utilization expanded since its baseline ranges in 2023. Crypto card volumes reached over $1.5B in month-to-month settlements as of August 2025.

Playing cards linked to stablecoin balances are attempting to supply a seamless expertise based mostly on standard card utilization patterns. The expansion of crypto playing cards put fee suppliers like Exa and Gnosis Pay consistent with standard credit score and debit card utilization. The common measurement of funds for Exa was akin to US debit card spending.

P2P funds didn’t see any huge modifications or new developments. These varieties of funds had a decrease common transaction measurement. The common measurement of P2P funds was decrease in comparison with Zelle and Venmo. Total, P2P is among the many riskiest usages for stablecoins, as customers flocked to curated apps.

Stablecoins are nonetheless extensively utilized in scams, and solely a fraction of the stolen funds is frozen or returned.