An almost $150 million prediction market has devolved into chaos after the platform Polymarket moved to disclaim payouts to merchants who precisely predicted that company treasury agency Technique would promote a portion of its Bitcoin holdings.

The dispute facilities on a elementary disconnect between when an occasion happens and when it’s publicly disclosed, exposing structural flaws in how decentralized prediction markets resolve multibillion-dollar wagers. Bettors at the moment are locked in a bitter dispute over a technicality that would wipe out thousands and thousands of {dollars} in payouts merchants believed had been assured.

On June 1, Technique, the enterprise intelligence agency previously often called MicroStrategy, which holds practically $60 billion of the highest crypto asset, filed a regulatory doc confirming it offered 32 Bitcoin, valued at roughly $2.5 million, between Could 26 and Could 31.

Technique offered 32 BTC to pay dividends – However the actual threat is what occurs if it has to promote extra Bitcoin

Technique’s first Bitcoin sale in practically 4 years reveals how its treasury might turn out to be a funding supply for the credit score merchandise constructed round it.

For individuals in a Polymarket contract asking whether or not Technique would promote any of its Bitcoin by Could 31, the 8-Okay submitting seemed to be definitive proof of a “Sure” consequence.

Nevertheless, the market is at the moment navigating a contested decision course of that closely favors “No.”

Polymarket directors issued a post-deadline clarification stating that, as a result of the general public affirmation of the sale didn’t emerge till June 1, the transaction doesn’t qualify below the platform’s operational customs.

The scenario has sparked widespread allegations of market manipulation, drawing intense scrutiny to the mechanics of decentralized betting at a time when prediction platforms are striving for mainstream monetary legitimacy.

The timeline of the contested Polymarket commerce

The continued controversy stems from the contract’s particular wording, which acknowledged that the market would resolve to “Sure” if Technique offered any of its Bitcoin by 11:59 p.m. ET on Could 31.

The foundations explicitly designated the corporate’s public disclosures and on-chain knowledge as the first sources of decision.

When Technique filed its necessary 8-Okay disclosure on June 1, the market remained open for energetic buying and selling. Observing that the agency had executed a sale objectively earlier than the Could 31 deadline, a number of merchants rushed to capitalize on what they perceived as a pricing inefficiency.

One market participant, working below the pseudonym willo2, staked $527,000 on “Sure” after studying the regulatory submitting. As a result of the market was pricing the chances of a sale at round 80 cents on the greenback even after the disclosure, the dealer anticipated a 20% arbitrage alternative.

As a substitute, the dealer misplaced your complete half-million-dollar principal. Following the inflow of capital, Polymarket added a clarification to the market description, stating that confirmations outdoors the desired timeframe wouldn’t be honored.

Talking on these occasions, Willo wrote on X:

“This was straight-up NOT a part of the principles. It was not written down in the marketplace, it didn’t make sense – and most of all, Polymarket did not even imagine it themselves. Why? As a result of if it was true, the market would have closed on Could thirty first. The market did not shut.”

Market analysts have broadly condemned the sequence of occasions. Jeff Dorman, chief funding officer on the digital asset administration agency Arca, identified a crucial logical inconsistency within the platform’s dealing with of the timeline.

Dorman famous that if the contract’s strict parameters dictated an finish exactly at midnight on Could 31, the platform ought to have halted all buying and selling at that precise second.

In line with him, permitting individuals to proceed shopping for shares on June 1 whereas retroactively implementing a Could 31 affirmation deadline created a entice for merchants counting on conventional authorized interpretations of the contract textual content.

Jonatan Pallesen, a knowledge scientist who displays decentralized platforms, characterised the platform’s habits as a type of fraud by omission.

Pallesen argued that whereas requiring information affirmation to align with the occasion deadline is an inexpensive safeguard towards indefinite market delays, failing to explicitly codify that customized within the contract guidelines exploits retail bettors.

Institutional merchants conversant in the platform’s unstated conventions had been in a position to extract vital capital from customers who moderately assumed {that a} accomplished sale meant a profitable ticket.

The UMA oracle vulnerability

The Technique dispute has escalated from a single contract right into a referendum on Polymarket’s underlying settlement structure.

Not like conventional monetary exchanges that depend on centralized clearinghouses and authorized compliance departments to settle derivatives, Polymarket outsources its truth-finding to Common Market Entry (UMA).

UMA operates as an “optimistic oracle,” a decentralized community the place token holders vote to resolve disputed outcomes.

Below this framework, any consumer can problem a proposed market settlement by staking a $750 bond. If the end result is contested a number of occasions, the choice defaults to a vote by UMA cryptocurrency holders.

The last word payout is set by the load of tokens solid, slightly than an goal judicial assessment of the info.

Critics argue that this method is extremely susceptible to manipulation. Eric Conner, a outstanding cryptocurrency analyst, famous that the token-voting mannequin is structurally compromised.

Conner argued that giant token holders, sometimes called whales, can weaponize ambiguous contract guidelines to guard their very own monetary positions and override goal actuality to forestall large losses.

Latest knowledge assist these issues. A WSJ investigation into the platform’s voting mechanics revealed that the ten largest wallets account for greater than half of the votes in most Polymarket disputes.

Moreover, roughly 60% of energetic UMA voters had been straight linked to dwell Polymarket accounts, and one in 5 contested markets featured voters who held a direct monetary stake within the consequence they had been adjudicating.

Polymarket has already recorded over 1,150 disputed markets within the first 5 months of 2026, eclipsing its total whole for the earlier 12 months.

The platform itself has restricted recourse, as its decentralized construction technically prevents inner administration from overriding a finalized UMA token vote.

Mainstream development meets decentralized friction

The timing of the $150 million dispute is precarious for the prediction market sector, which has aggressively expanded its footprint into conventional finance and media over the previous few years.

Throughout this era, the platforms Polymarket and Kalshi have actively distanced themselves from being labeled as unregulated crypto casinos.

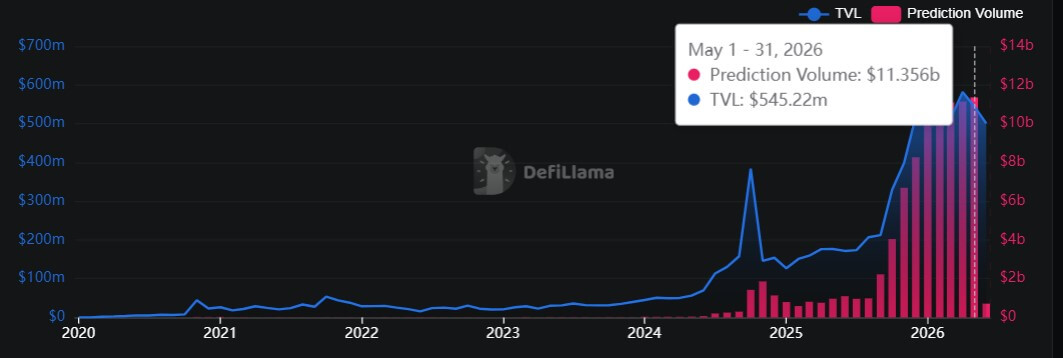

Nevertheless, they’ve seen their buying and selling quantity improve quickly to exceed $10 billion in Could 2026. This marks a tenfold improve from the identical interval final 12 months, per DeFiLlama knowledge.

On the similar time, they’ve established content material and knowledge integration agreements with main establishments, together with the New York Inventory Trade, Dow Jones, The Related Press, and Fox Information.

This fast institutionalization follows years of intense regulatory friction. In 2022, the Commodity Futures Buying and selling Fee (CFTC) compelled Polymarket to close down its US operations and relocate overseas.

Kalshi subsequently engaged in a chronic authorized battle with the CFTC over the best to host political occasion contracts, finally profitable a landmark federal courtroom case in late 2024.

Nevertheless, the regulatory surroundings shifted after the 2024 presidential election, which the platforms accurately predicted could be a Donald Trump victory.

Since then, the platforms have loved vital regulatory backing, with Polymarket buying a federally licensed derivatives trade, and the CFTC additionally asserting its unique proper to control these markets.

CFTC Chairman Michael S. Selig stated:

“Occasion contracts permit companies and people to hedge event-driven dangers, allow traders to handle portfolio publicity, and supply the general public with details about the end result of future occasions. These merchandise are commodity derivatives and squarely throughout the CFTC’s regulatory remit.

Regardless of securing regulatory footholds, the basic mechanics of decentralized prediction markets stay extremely experimental.

In conventional fairness markets, deep liquidity and strict regulatory oversight usually be certain that asset costs mirror materials actuality.

On platforms ruled by tokenized voting programs, the definition of actuality remains to be up for debate.

Till these structural dispute mechanisms mature, merchants navigating the booming prediction market financial system stay on the mercy of unwritten guidelines and decentralized juries.